By John Richardson

WHEN CORONAVIRUS first became a pandemic, I flagged- up that government intervention would play a critical role in shaping petrochemicals.

This proved to be the case as government cheques in the developed world were spent on computers, game consoles, washing machines and refrigerators made in China that were manufactured from domestically produced and imported petrochemicals and polymers.

The tide that lifted China’s economic boat, as it recovered from the pandemic in H2 2020, was hugely beneficial for the whole of the global petrochemicals business.

The nature of developed-world government stimulus was also very different than during the Global Financial Crisis (GFC).

During the GFC, lower-paid workers were left to largely carry the can for sub-prime lending errors as the “too big to fail” banks were bailed out.

In 2020 and 2021, money flowed into to job furlough and income support schemes that left some lower-paid workers better off during the pandemic than before it began.

Combine this with all the extra polymers consumption that came from people eating more supermarket food and less in restaurants (increased “surface area” demand) and the boom in internet sales (online deliveries use a lot of plastic packaging), and this explains why demand for resins such as polyethylene (PE) performed extremely well relative to the declines in GDP.

Further demand support came from all the syringes, personal protective equipment, face masks and medical packaging required to combat the pandemic.

I therefore don’t buy the view that the Ukraine-Russia conflict has interrupted a petrochemicals industry recovery that would otherwise have gained lots more momentum this year.

In several key end-use sectors such as white goods, electronics and packaging, there was no real downturn in the first place. Without a downturn there cannot be a recovery. Hence, I see it as misleading to talk about the Ukraine-Russia conflict stalling a recovery in 2022.

Here are two examples of how well petrochemicals performed relative to GDP in 2020, based on ICIS Supply & Demand data:

- US linear low-density PE (LLDPE) demand grew by 1% in 2020 over 2019 despite a year-on-year 4% fall in GDP. This was an incredibly strong performance when you consider that in 2008 over 2007, during the GFC, US LLDPE demand fell by 16% despite only a 0.1% decline in GDP.

- EU plus UK demand also grew by 1% even though GDP contracted by 6% in 2020 over 2019.This is best compared with 2009, the low point of the EU sovereign debt crisis (the UK was, of course, still an EU member then). Year-on-year LLDPE demand fell by 10% as GDP declined by 5%.

In 2021 over 2020, US LLDPE demand grew by a further 6% as GDP growth returned to a positive 4%. The EU plus the UK saw a 6% LLDPE demand growth and a 6% rise in GDP.

Patterns of demand growth versus GDP were very similar in several other major petrochemicals and polymers.

New drivers of developed-world petrochemicals demand

With this misconception out of the way, let me move onto some preliminary thoughts about the impact of the Ukraine-Russia conflict on petrochemicals demand in the developed world.

On 13 February, I focused on what I believed were the factors that would drive PE demand in 2022 in the developed world and China. Some must not all of the factors have been changed by Ukraine-Russia.

I hope what follows helps as a first pass at describing the new environment in which our industry is operating, as I focus here only on the developed world. I will revisit China in a later post. I discussed the developing world in my post on 23 March.

Underpinning the revised demand drivers – which this time I see applying to all petrochemicals and polymers -– is my belief that there will be no quick resolution to the crisis. Let’s hope I am wrong.

Here goes:

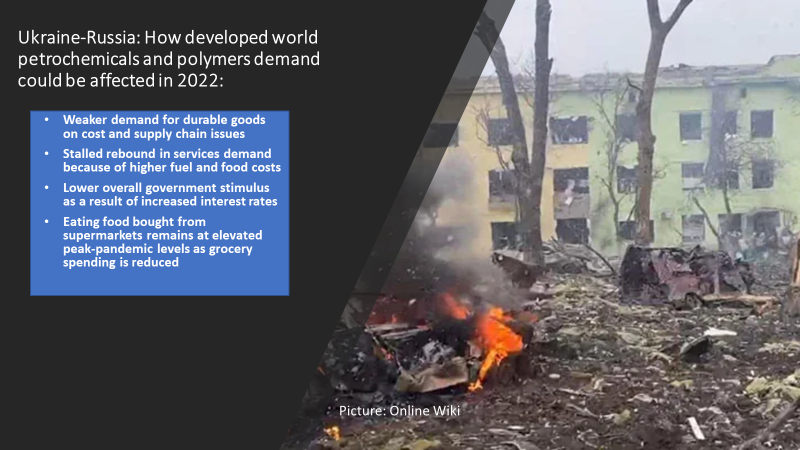

- Weaker demand for durable goods on cost and supply chain issues. More microchip shortages and further container-freight disruptions are likely to affect autos demand. But workarounds include Ford planning to sell cars without chips – with missing parts supplied within a year, according to ICIS downstream demand analysis. Companies including Tesla are looking at selling cars without USB ports or other non-security-related features. Chip shortages are also affecting white goods sales. But the biggest impact on durable goods demand will surely be affordability and not supply.

- A stalled rebound in services demand. The endemic phase looked set to result in a rebound in petrochemicals demand related to travel and attending concerts and theatres etc. But the rise in fuel and food costs now represent a threat to this recovery.

- Lower overall government stimulus. Higher interest rates make the kind of huge broad-based stimulus we saw at the height of the pandemic much more difficult. But targeted relief for low–paid workers as compensation for higher food and fuel costs is already happening.

- The extent to which online spending has moved permanently higher because of shopping habits developed during the pandemic and greater investment in sectors such as food delivery, leading to improved convenience. Despite the sustainability pressures, a lot of plastics packaging is used in online sales. We need to evaluate whether higher fuel costs will now affect internet sales.

- Eating food bought from supermarkets may stay at peak-pandemic levels. Before the Ukraine-Russia conflict, it looked as if the endemic phase of coronavirus would lead to a boom in spending in restaurants, thereby reducing “surface area” demand as grocery spending in supermarkets declined. But big increases in the cost of living look likely to limit dining out. Don’t assume this will maintain food packaging demand at peak-pandemic levels, as we could see people cutting back on their grocery spending. This could happen even in the developed world where food-packaging demand is normally unaffected by economic circumstances. We haven’t seen inflation at these levels since the 1970s.

- As offices reopen, a recovery in demand connected with travelling to work and city centre sandwich bars and restaurants. But people would be spending less time in neighbourhood sandwich bars and restaurants.

- A fall in hygiene-related demand if coronavirus becomes endemic. But to what degree will precautions against infection remain mandated such as wearing face masks? And has human behaviour become a lot more infection-cautious?

- BUT we may see a resumption of lockdowns if a new variant is more virulent than Omicron. UK scientists warn there are no guarantees of declining virulence. This could maintain demand in hygiene applications.

- More plastics recycling, Ukraine-Russia may add to the sustainability push as recycling is “local for local”. Plastic rubbish cannot be moved long distances for cost and environmental reasons. If production chains are entirely local, they are not at risk of geopolitics-related supply disruptions.

Conclusion: Upstream integration, transfer pricing and the broken GDP tool

If you are a petrochemicals company with internal access to most if not all your hydrocarbon feedstocks, your cost pressures may not be that bad.

Perhaps your upstream naphtha and LPG supplier will help share the huge profits being made from soaring energy prices through more favourable transfer pricing. Perhaps not. This will hinge on internal and often non-transparent transfer pricing mechanisms.

But for the standalone petrochemical companies with little or no access to internal feedstocks, this is a cost crisis on an historic scale.

When it comes to petrochemicals demand – as I have argued above – the outlook is extremely complex. This underlines why multiples over GDP no longer work as a methodology for assessing petrochemicals demand.

Understanding demand requires deep and constant end-use by end-use analysis, leading to far more flexible sales and plant operating tactics than has been the case in the past.

And as this crisis morphs into what I believe will be a long-running Cold War, new demand opportunities will emerge as globalisation goes into reverse and the world splits into two manufacturing blocs. More on this in later posts.