China accounted for 33% of global growth in the seven major synthetic resins between 1990 and 2001. But this jumped to 63% in 2002-2021. In distant second place during both these periods was the Asia and Pacific region at 15% and 17% respectively.

Asian Chemical Connections

China could become the world’s third-biggest PP net exporter in 2022-2040

China’s cumulative net imports of polypropylene (PP) might be as big as 91m tonnes in 2022-2040 – the ICIS base case. Or China’s total net exports during the same period may reach 90m tonnes.

Success in the new HDPE world: Tactics must be accompanied by a whole new strategy

By John Richardson TACTICALLY, as the first chart below tells us, using just high-density polyethylene (HDPE) as an example (the same applies to other grades of PE and polypropylene), it is obvious what the major exporters in the Middle East and elsewhere must do as China’s self-sufficiency increases. The exporters need to focus on import […]

This is the first significant chemicals downcycle for many years

Every tonne of polymer you decide not to produce because there isn’t a viable market will save vital revenues – especially as feedstock costs will remain very volatile. Every tonne of polymer you do produce because the market works will earn you crucial money at a time of declining overall sales.

Global PE and PP indexes Week Two: Asian prices recover as Europe declines continue

THESE ARE STILL extraordinary times in global polyolefins markets. Although the great equalisation has begun as pricing in most of the rest of the world falls towards Chinese levels, price premiums over China remain historically very high. There are thus still strong opportunities for exporters to make good netbacks in markets other than China.

European PE and PP producers face re-globalisation risks

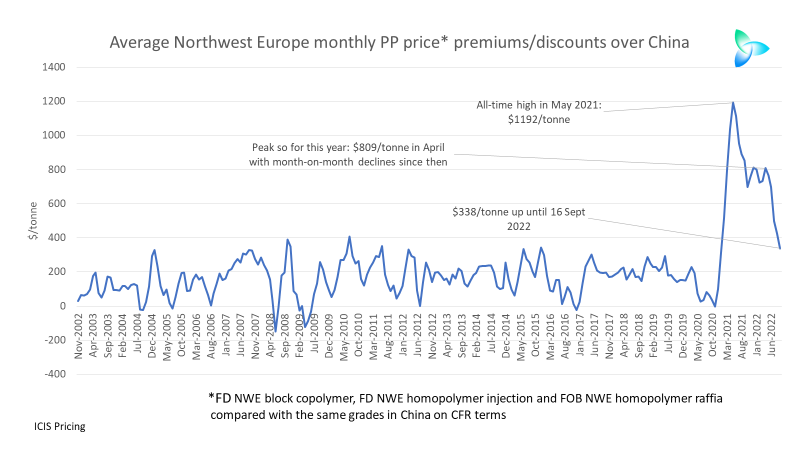

Northwest Europe PP price premiums over China averaged $161/tonne between November 2002 and December 2020. Between January 2021 and 16 September 2022, price premiums averaged $749/tonne. What would be the consequences for European PP pricing and profitability if price premiums returned much closer to their long-term averages?

A perfect global PP storm: China’s collapsing demand and rising capacity

THIS IS A POLYPROYPENE ((PP) world being turned upside down. China has entered a period of lower growth with capacity additions so big that imports are collapsing as China also starts to substantially increase exports.

If you think this is a typical chemicals downcycle, think again

THERE IS A FEELING out there that the chemicals and polymers industry is undergoing a typical downcycle that will last a few years, followed by yet another spectacular fly-up in margins. But I believe a great deal more is happening beyond the usual cycles of over-building followed by under-building.

Latest China PP spreads, margin and demand data show market remains at multi-decade lows

The average China PP price spread in 2022 up until 19 August, was just $262/tonne. This compares with the previous annual record low of $430/tonne in 2003.

The rules of the chemicals game are changing as companies pay the penalty for “growth for growth’s sake”

Because companies in all manufacturing and service sectors haven’t been adequately charged for the natural resources they use, and the damage they cause to the environment, we face the risks of catastrophic climate change and more plastic in the oceans than fish.

Jump to page: