THERE IS A FEELING out there that the chemicals and polymers industry is undergoing a typical downcycle that will last a few years, followed by yet another spectacular fly-up in margins. But I believe a great deal more is happening beyond the usual cycles of over-building followed by under-building.

Asian Chemical Connections

The rules of the chemicals game are changing as companies pay the penalty for “growth for growth’s sake”

Because companies in all manufacturing and service sectors haven’t been adequately charged for the natural resources they use, and the damage they cause to the environment, we face the risks of catastrophic climate change and more plastic in the oceans than fish.

Global chemicals: What I believe our industry must do in response to a deep and complex crisis

I WORRY that we face a crisis deeper and more complex than any of us have seen before because of the confluence of geopolitics, demographics, the changing nature of the Chinese economy as Common Prosperity reforms accelerate, China’s rising chemicals and polymers self-sufficiency, the high levels of global inflation with all its causes, and, last but certainly not least, climate change.

Europe’s gas crisis: the implications for global chemicals

GEOPOLITICS IS, I believe, just one aspect of a crisis facing the chemicals industry that is deeper and more complex than anything we have faced before.

Front mind right now in geopolitics is Ukraine-Russia and the gas-supply crisis facing Europe,

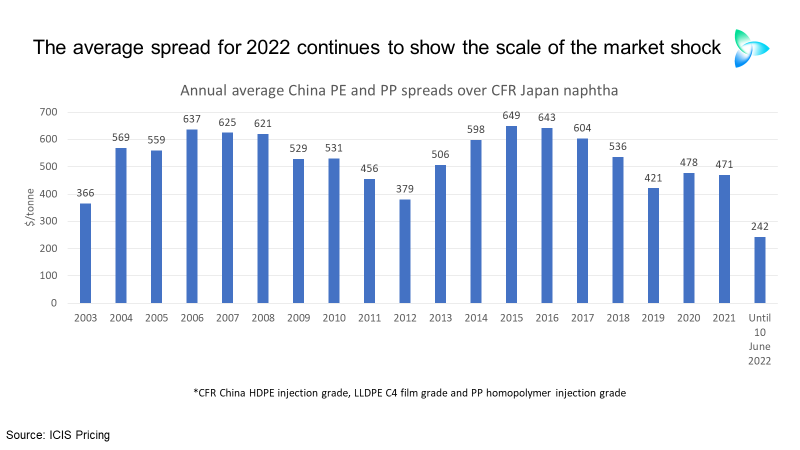

China’s latest LLDPE spread and demand data offer worrying clarity about the broader economy

THE LATEST DATA on linear low-density polyethylene (LLDPE) China CFR (cost & freight) pricing spreads over CFR Japan naphtha costs underlines the evidence from the other grades of polyolefins, that China is a long way from a full economic recovery.

Polyolefins pricing data suggest China still hasn’t recovered

Comparative PE and PP pricing data between Vietnam and southeast asia – and the “spreads” numbers between China PE and PP prices and naphtha costs – suggest the China economy has yet to recover.

China naphtha-to-polyolefins spreads data still show recovery yet to happen

RECOVERY? WHAT RECOVERY? Some market players are talking about a rebound in the Chinese economy, and, therefore, polyolefins demand, but the critically important spreads data continue to tell a different story. Nothing has changed from last week.

China’s post-lockdown economic rebound has yet to happen, according to the ICIS spreads data

At some point, polyolefins exporters to China and the local producers will regain pricing power. This will become apparent from a widening of spreads as economic activity returns to normal. It really is as simple as this. So, you need our data and analysis.

European polypropylene: Supply chain demand destruction and the need for a new business model

EFFICIENT SUPPLY CHAINS were something that we used to take for granted. They hummed away in the background, making petrochemicals just one of many globalised industries where products and services flowed almost seamlessly across borders. We didn’t have to think about supply chains because they worked so well.

Big divergence between Europe PE and PP markets continue, creating seller and buyer opportunities

REGULAR readers of the blog will know that I first highlighted the big polyolefins market divergence in April 2021. Back then, I said that:

Asia and Middle East producers needed to sell more to Europe.

Buyers should secure more resin supplies from Asia.

Jump to page: