IT ALL CHAOS AND MUDDLE out there: China’s ethylene glycols demand could either grow by 10% in 2023 or contract by 5%.

Asian Chemical Connections

A flood of PP no matter how what the 2023-2025 demand growth

EVEN if China’s PP demand growth is 14% this year – double our forecast – and growth in other regions is higher than we expect:

Global capacity in excess of demand would be 18m tonnes in 2023 compared with a 8m tonne/year average in 2000-2022,

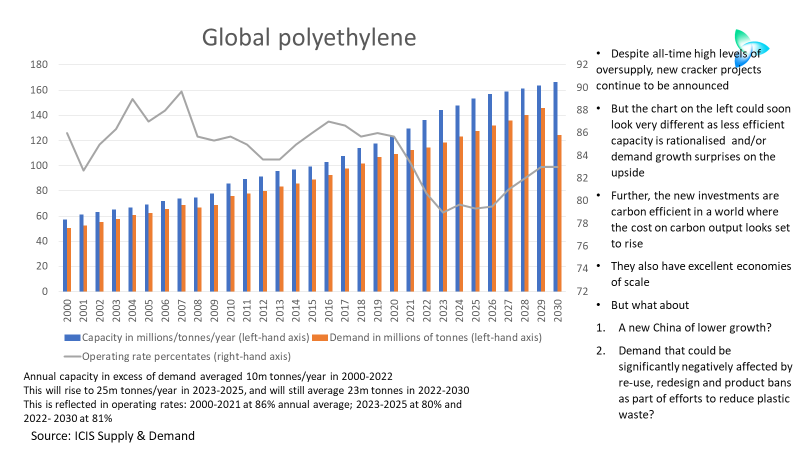

Global PE new supply and China spreads tell the real story

Global PE capacity in excess of demand is forecast to average 24m tonnes/year in 2022-2025, and to reach 26m tonnes this year

Operating rates are expected to average 81% in 2022-2025. This would compare with a 10m tonnes annual average capacityexceeding demand in 2000-2021 and an operating rate of 85%.

Your complete and updated outlook for global polyethylene in 2023

The strength of China’s post zero-COVID recovery in 2023 will be crucial, as will local operating rates as self-sufficiency further increases.

Another important factor: European gas supply next winter and the effect on local PE production.

Assessing confidence and the China PE demand recovery: More scenarios are needed

Scenario 2, my preferred scenario, would see China 2023 PE demand at approximately 38.5m tonnes – an average of 2% higher across the three grades than in 2022.

Cracker project announcements continue despite all-time high oversupply

Companies behind the crackers due on-stream over the next four years emphasise the low-carbon output. The planned new plant also have excellent economies of scale

Coming to terms with the new China is essential for sensible forecasting

Even our base case sees global PE capacity in excess of de</mand at 22m tonnes in 2023 compared with a 10m tonnes/year annual average in 2000-2022. We forecast this year’s global operating rate at 79% versus the average annual 2000-2022 operating rate of 86%. Downside One would see 28m tonnes of excess capacity and a global operating rate of 77%; Downside Two would be 30m tonnes and 76% respectively.

China polyolefins in 2023: Demand and supply workshops crucial

This year is a great deal harder to predict than 2022,, hence my latest outlook for China’s PP demand (see the chart below), which includes the two extremes of our ICIS base case for 6% growth versus my worst-case downside of minus 5%.

China PE market in 2023: Recovery threatened by economic inequality, real estate decline

Under Scenario 1, China’s PE demand in 2023 would total 39.1m tonnes, 4% higher than last year; Scenario 2 would see demand at 36.4m tonnes, 3% lower; and Scenario 3 would involve a contraction of 5% to 35.7m tonnes.

China HDPE 2023 demand and net import forecasts

Scenario 1 for next year assumes that China successfully transitions from its zero-COVID policies. Consumer confidence comes roaring back. Demand grows by 4% year-on-year to a market of 17.6m tonnes.

Scenario 2 assumes that high infection rates and lack of healthcare resources keep consumer confidence depressed but that the global economy recovers, supporting China’s exports. Growth is minus 2%, leaving demand at 6.6m tonnes.

The worst-case outcome is Scenario 3 where the impact of zero-COVID continues, and the global economy gets weaker. Consumption falls by 4% to 16.1m tonnes.

Jump to page: