UNTIL I FULLY understood the potential supply and industry economics implications of converting a lot more oil into petrochemicals, what’s happening to demand and the extent of China’s future self-sufficiency, I used to present charts such as the one above to clients with the proviso: “The good news is that this chart will almost certainly be wrong”. NOW I AM NOT SO SURE

Asian Chemical Connections

The scale of plans to turn oil into petrochemicals may radically reshape this industry

A petrochemicals world dominated by Supermajors, especially those running COTC plants, or one where greater regional cooperation (more on this in later posts) and increased protectionism allow older, smaller and less carbon efficient plants to survive.

A fundamental shift in thinking on petrochemical plant closures

Environmental, social and political factors – along with integration into upstream petrochemicals – have held back plant closures. Now, things seems very different.

Overstocking may have boosted China PE demand as the US continues to win while others lose

THE US gains $296m in China HDPE sales as Asian and Middle East exporters lose $1.4bn.

Big HDPE exporters see another $700m of estimated China sales losses in one month

NINE OUT OF CHINA’S top 10 high density polyethylene (HDPE) import partners saw their sales to China fall by an estimated total of $1.8bn in January-July 2023 versus the same period last year. Meanwhile, the remaining member of the top 10, the US, saw its sales increase by $233m.

Global HDPE capacity may have to be 13m tonnes/year lower in 2024-2030 to return to healthy operating rates

Global HDPE capacity in 2024-2030 would need to be a total of 13m tonnes/year lower than our base case to return to the 2000-2019 operating rate of 88%.

An almost perfect LLDPE buyers’ market as major producers see big China sales declines and losses in export volumes.

SEE ABOVE estimated LLDPE H1 2023 sales in China versus average H1 1999-2022 sales. Total estimated losses amounted to $594m among some of the big global producers.

Global PP crisis: Why capacity may need to be 18m tonnes/year lower in 2024-2030

GLOBAL PP capacity may have to be a total of 18m tonnes/year lower in 2024-2030 to return operating rates to the historically strong levels

China H1 2023 PE market review and outlook for the second half

CHINA’S PE demand is heading for 1% growth this year based on the H1 2023. data. Northeast Asian margins would have to recover by 3,423% to get back to normal.

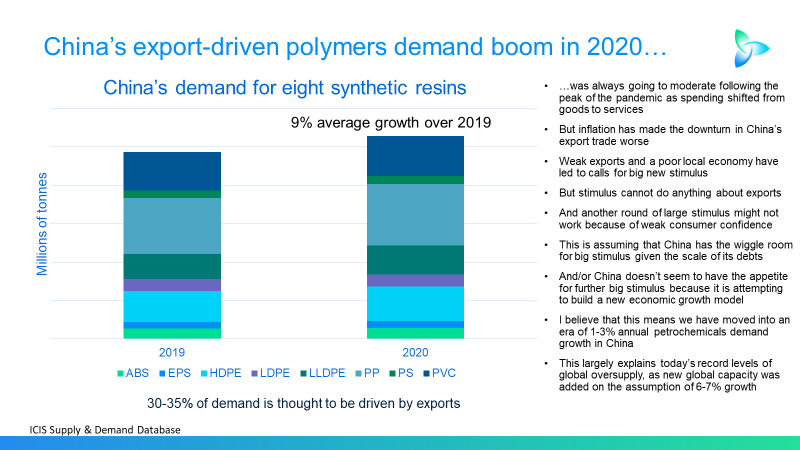

China and “pushing on a piece of string: The moderate impact of future economic stimulus

THE PHRASE “pushing on a piece of string” might best describe the logic behind calls for another round of big economic stimulus in China. Any extra money pumped into the economy could be largely saved rather than spent because of weak consumer confidence resulting from an ageing population and the end of the property bubble.

Jump to page: