Comparative PE and PP pricing data between Vietnam and southeast asia – and the “spreads” numbers between China PE and PP prices and naphtha costs – suggest the China economy has yet to recover.

Asian Chemical Connections

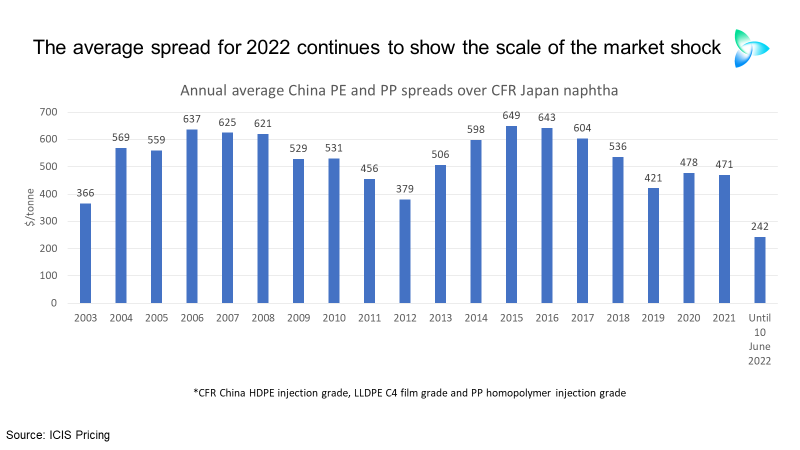

China naphtha-to-polyolefins spreads data still show recovery yet to happen

RECOVERY? WHAT RECOVERY? Some market players are talking about a rebound in the Chinese economy, and, therefore, polyolefins demand, but the critically important spreads data continue to tell a different story. Nothing has changed from last week.

China 2022 PE demand: latest data point towards a 2% contraction as confusion over outlook builds

January-April 2022 data point towards China’s polyethylene demand for the full year declining by 2% over 2021.

China’s post-lockdown economic rebound has yet to happen, according to the ICIS spreads data

At some point, polyolefins exporters to China and the local producers will regain pricing power. This will become apparent from a widening of spreads as economic activity returns to normal. It really is as simple as this. So, you need our data and analysis.

China’s ethylene equivalent demand growth in 2022 could be as high as plus 9% or as low as minus 3%

Scenario 1, the ICIS Base Case, for China’s ethylene equivalent demand, sees growth at 9% in 2022 over last year. Scenario 2 involves 4.5% and Scenario 3, minus 3%.

PE and PP production decisions become super-critical amid Ukraine-Russia, zero-COVID complications

Every tonne you don’t produce, when you correctly assess that the demand isn’t there in a particular market, will be important in preserving cashflow. Cashflow could once again be king, as it was just during the 2008-2009 Global Financial Crisis; and every tonne that you do produce, when you accurately assess that demand is there will, of course, support your revenues.

New scenarios for 2022 Eurozone and UK PE growth as inflation and debt pressures build

The ICIS Supply & Demand Base Case growth for Eurozone and UK PE demand in 2022 over last year is 1%. Downside 1 assumes consumption will contract by 4% and Downside 2 by 7%.

China polyethylene: latest scenarios for 2022 demand and net imports

China’s polyethylene (PE) demand in 2022 could fall by 3% over last year. Net imports may be as much as 3.9m tonnes lower

China’s 2022 PE growth may be minus 3% with net imports declining by 29%

I AM JUST about clinging to a base case of positive China polyethylene (PE) demand growth in 2022 because China has a great track record of turning its economy around after short periods of weaker growth. But this time could be different.

Europe petrochemicals demand weakness may have bigger impact than any production cuts

Lower refinery operating rates on a lack of Russian oil and naphtha -– and reduced electricity supply to refineries and petrochemicals plants -– may be more than offset by weaker European petrochemicals demand.

Jump to page: