ICIS Power Perspective: Germany’s coal phase-out a burden for European power markets? – an impact analysis

ICIS Editorial

26-Apr-2019

This story has originally been published for ICIS Power Perspective subscribers on 24 April 2019 at 13:55.

The German government began talks in April with 11 neighbouring countries and the European Commission in anticipation of a planned coal exit in the country by 2038. Energy minister Peter Altmaier said that close coordination with neighbouring countries will be important to avoid high power prices and ensure security of supply in the region.

Germany plans to phase out all coal and lignite-fired power before 2038 if the country’s cabinet and legislature accepts recommendations made in the final report by a government-appointed commission that was published in January 2019.

This could significantly tighten European supply margins and drive up wholesale power prices across the region. Our modelling suggests that a German coal phase-out will increase exports from France and Netherlands to Germany and convert Poland from a net importer to a net exporter.

For European power prices, a German coal phase-out is clearly bullish, with an average price increase across all directly interconnected markets of €0.2/MWh for the 2019 to 2022 period and €2.2/MWh for the period 2023 to 2030. The Nordics and the Netherlands see the highest power price increase due to the strong use of interconnectors to minimise price differentials, whereas power prices in Poland and UK will be the least affected.

Background

- Coal and lignite-fired electricity accounted for around 40% of power output in 2018

- ICIS forecasts higher German power prices if coal exit proposals are written into law with the highest prices and tightest supply expected between 2023-2025

- The German coal exit process is driven mainly with climate targets in mind, such as 65% generation from renewable sources before 2030. Germany is unlikely to meet its 2020 targets

- Energy minister Altmaier said following the coal exit report that he did not want Germany to rely on nuclear imports from neighbouring countries to ensure security of supply

- Though appointed by the government, the agreement of the expert commission is non-binding and remains a recommended proposal. A draft coal exit law should be ready for debate by late autumn

- All countries set for talks except Poland and Czech Republic have plans to phase out coal or have already phased out coal

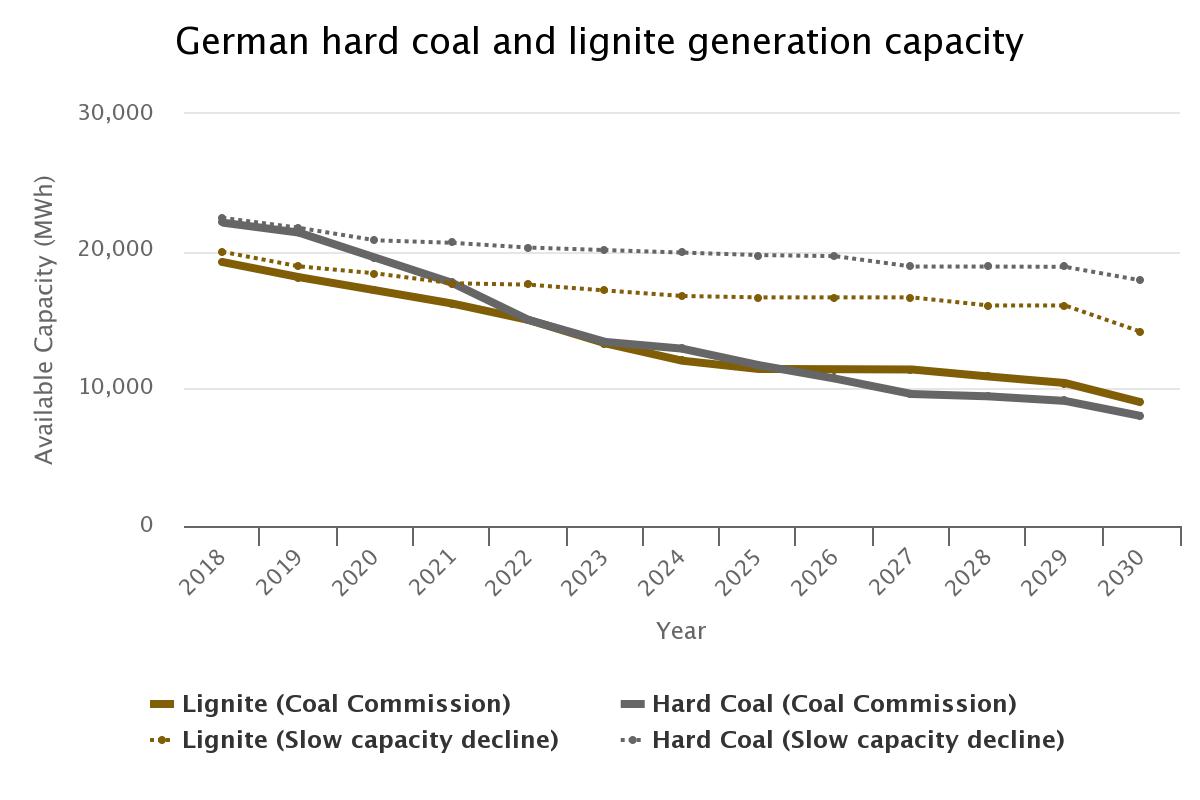

Scenario set-up

- In order to simulate the impact of the

proposed coal phase-out by Germany’s expert

commission on the neighbouring power markets,

we have designed a comparison of two model runs

- “Coal commission”: The reduction of

German coal and lignite capacity in line

with the recommendations proposed by the

German expert commission

- Coal and lignite-fired capacity

will be phased out in three steps by

2038. The commission outlined the

following plan in three stages.

- 2022: 15GW hard coal and 15GW lignite

- 2030: 8GW hard coal and 9GW lignite

- 2038: 0 GW hard coal and lignite

- “Slow capacity decline”: Capacity

declining over a long timeframe

assuming a run-time of 50+ years for

lignite and hard coal assets

- 2022: 20.3GW hard coal and 17.6GW lignite

- 2030: 17.9 GW hard coal and 14.1GW lignite

- The capacity pathways are depicted in the chart below

- Coal and lignite-fired capacity

will be phased out in three steps by

2038. The commission outlined the

following plan in three stages.

- “Coal commission”: The reduction of

German coal and lignite capacity in line

with the recommendations proposed by the

German expert commission

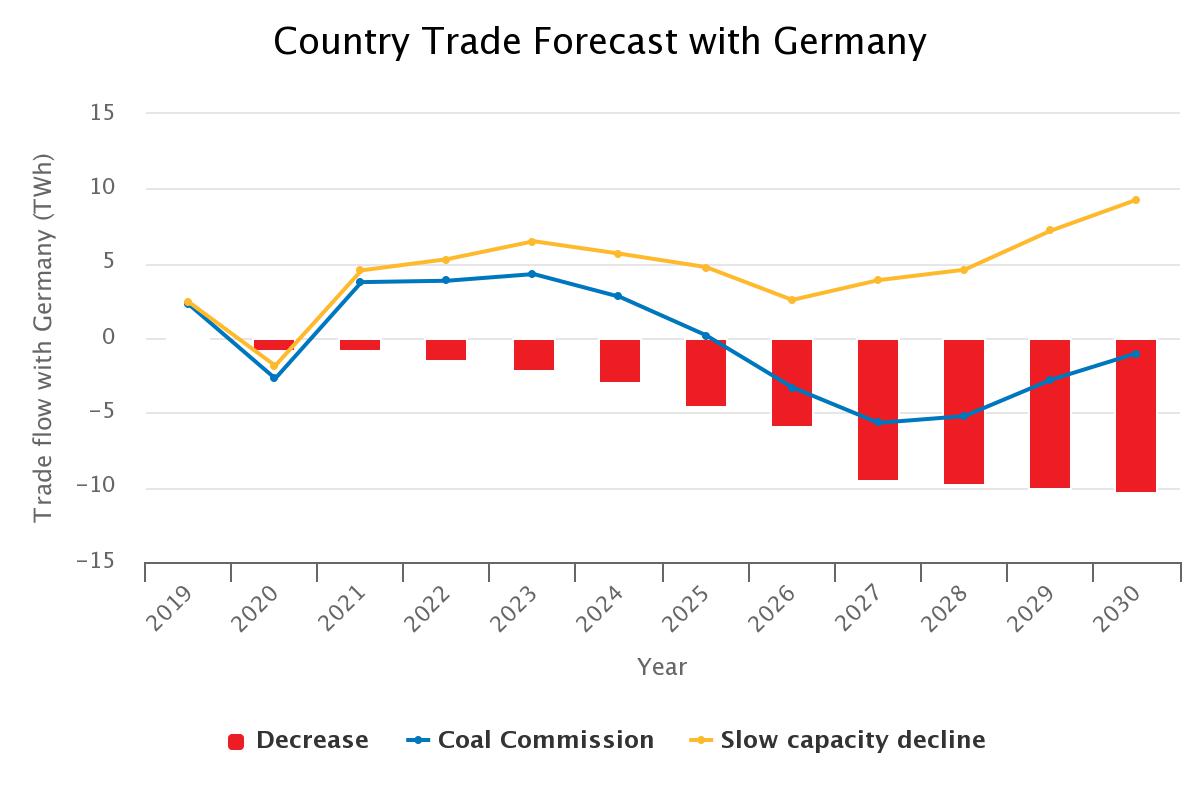

Impact on

cross-border trade

Impact on

cross-border trade

- All neighbouring countries should see lower imports from or higher exports to Germany in a coal phase-out scenario compared with a slow capacity decline scenario

- France will see a high increase in its exports to Germany after 2023, following the German nuclear phase-out. This increase will be significantly steeper when combined with a German coal phase-out with a delta between the scenarios increasing from 3TWh in 2023 to 8.5TWh in 2030

- A similar effect is visible for the Netherlands, which briefly turns into a net-importer from Germany in 2023 in the slow capacity decline scenario while in the coal phase-out scenario, Netherlands remains a net exporter to Germany for the entire 2019 to 2030 period. The delta between the scenarios increases from 4TWh in 2022 to 11 TWh in 2029 before relaxing slightly to 8.5TWh by 2030

- For Poland, the delta between the two scenarios is less pronounced, however the country will import from Germany as of 2022 until 2030 in the slow capacity decline scenario, whereas it switches to an exporter to Germany for the years 2028 to 2030 in the coal phase-out scenario

- The chart below shows Germany’s trade balance with France

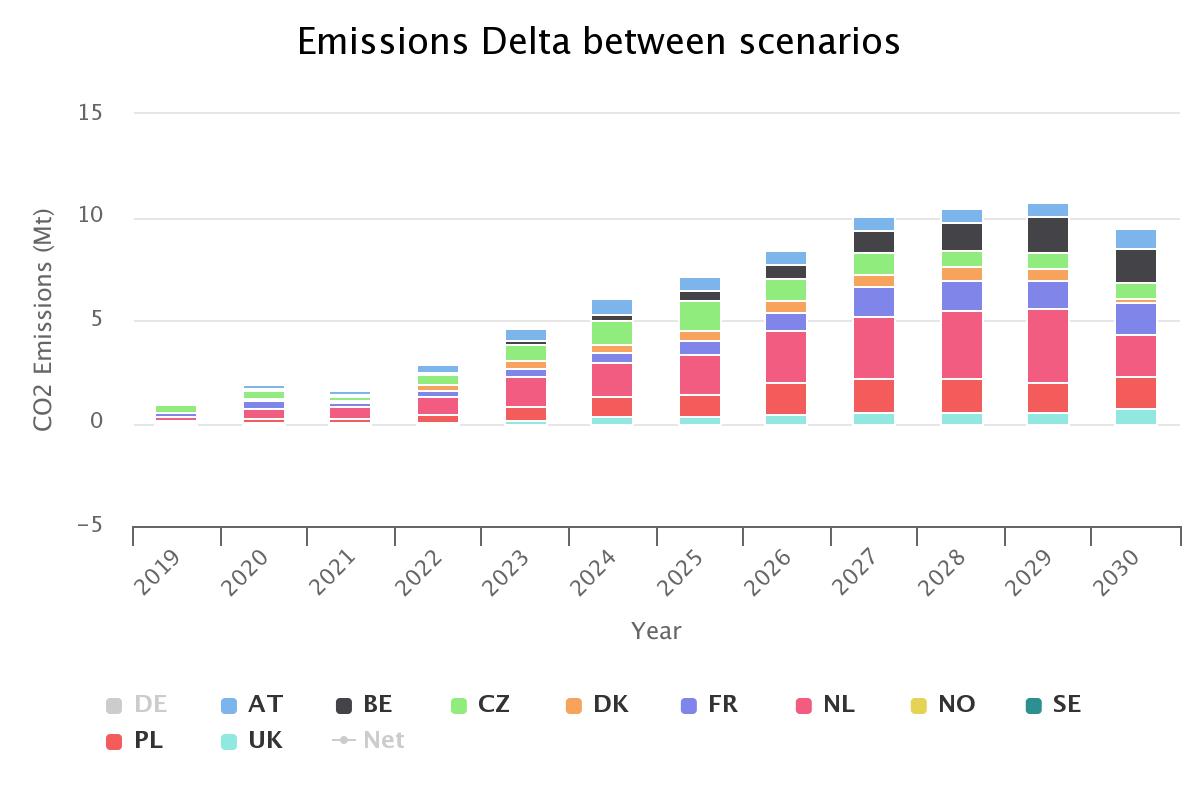

Impact on

emissions

Impact on

emissions

- With a coal phase-out we would see net emissions decrease by around 300m tonnes over the period 2019 to 2030, when combining Germany’s decreasing emissions (-371m tonnes) and the increase in emissions of neighbouring countries as a result of the proposed German coal phase-out

- Most of the increase is provided by higher generation in the Netherlands (+22m tonnes), Poland (+11m tonnes) and France (+9m tonnes)

- That means, over the period 2019 to 2030, Germany would have to cancel around 300m EUAs in order to mitigate the bearish effect on European carbon prices resulting from a German coal phase-out

Impact on European

power prices

Impact on European

power prices

- Part of the lower European electricity generation resulting from a German coal phase-out would be replaced by gas generation. This would tighten the trade balance across all 11 countries with Germany lowering its export levels especially from 2023 onwards in a coal phase-out scenario compared with a slow capacity decline

- As a result, German power prices are expected to increase in a coal phase-out scenario compared to steady decline, given the lower availability of thermal generation. The spread between the scenarios ranges around levels of €0.5/MWh until 2023, before steadily widening to as much as €6.7/MWh in 2030

-

- Despite a higher level of electricity export from France to Germany in a coal phase-out scenario, the French power prices should only marginally increase with coal capacity reduced across the border. French power prices would on average increase by €0.3/MWh between 2019 and 2026 before the spread between the scenarios widens to levels around €2.0/MWh until 2030

- Dutch power prices should see a steady increase in prices in a coal phase-out setting compared to a steady capacity decline, with levels around €0.4/MWh between 2019 and 2023. As a result of a German coal phase-out, the spread between the scenarios for Dutch power prices will increase to an average of €3.0/MWh for the period 2024 to 2030.

- The Nordic countries are affected on the bullish side with Germany’s phase-out plans increasing power prices for Norway, Denmark and Sweden by an average of €0.3/MWh for the period 2019 to 2023 and €3.1/MWh between 2024 and 2030 with Germany attracting higher electricity flows from the north to the south given the market’s price differential

- Traded spreads between the German and

French power baseload contracts for 2022

delivery have significantly tightened since

the coal exit report was published with

France falling to a discount on four

occasions in March 2019. Given that supply

gets tighter with the German nuclear

phase-out scheduled for 2023, prices are

expected to converge between the two

markets.

- In the slow capacity decline scenario, the French premium over the German prices is converging to zero Germany by 2024, slightly widening again to €3/MWh in 2028, before narrowing to zero again by 2030.

- In the coal phase-out scenario, the spread consistently narrows to zero until 2022. As Germany is expected to import more than current levels from France as of 2023 especially on days when renewable output is low, the spread will turn positive, with Germany trading at a €3/MWh premium over French power prices by 2030

Coal phase-out to increase likelihood of price spikes in Germany

- The below heat map compares the number

of hours in a certain price range for the

two scenarios for German hourly prices

between 2025 and 2030

- Negative numbers mean, that a higher number of hours was in a certain price-bin in the coal phase-out scenario compared to the slow capacity decline scenario

- There is a clear tendency that with the German coal phase-out there will be fewer hours with negative prices over time compared to the slow capacity decline scenario and an increasing number of higher priced hours and price spikes

Marcus Ferdinand is Head of European Carbon & Power Analytics at ICIS. He can be reached at Marcus.Ferdinand@icis.com

Zaheer Ahamed is Analyst – EU Carbon & Power Markets at ICIS. He can be reached at Zaheer.Ahamed@icis.com

Roy Manuel is Market Reporter at ICIS. He can be reached at Roy.Manuel@icis.com

Our ICIS Power Perspective customers have access to extensive modelling of different options and proposals. If you have not yet subscribed to our products, please get in contact with Justin Banrey (Justin.Banrey@icis.com).

As an analyst, trader or regulatory specialist now is the time to equip yourself with the latest trends in the market. The ICIS Carbon Seminar 2019 is the place for traders and analysts to discuss upcoming market developments.

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE