Asia’s petrochemicals face pressure from Saudi supply uncertainty

Nurluqman Suratman

19-Sep-2019

SINGAPORE (ICIS)–Key Asian petrochemicals are facing pressure from lingering uncertainty from Saudi supply amid geopolitical tensions in the Middle East.

Prices of these plastics have mostly risen since the recent attacks on oil facilities in Saudi Arabia on 14 September, along with global crude futures which edged higher on Thursday following days of volatile trade.

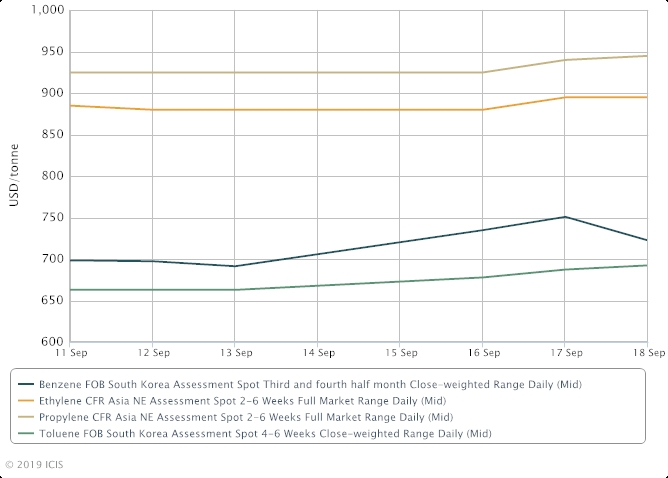

Asia’s benzene prices has gained cumulatively over $30/tonne, on a free-on-board (FOB) South Korea basis, in the initial trading days following the attacks, tracking crude futures in the same period.

At noon on Thursday, benzene prices were at $721/tonne FOB Korea, up from $691.50/tonne at the close on 13 September.

The rise in benzene prices has supported the sharp increase in maleic anhydride (MA) offers this week, with sellers keen to hold back until they have better clarity on upstream market conditions before finalising their offers.

Moreover, Saudi’s October contract prices for butane are expected to rise in the aftermath of the attacks, and as Saudi Aramco is the key butane supplier to Asia.

Asian makers of butane-based MA are eyeing substantially higher MA offers to compensate for the potentially steeper feedstock costs, market players said.

In Asia, toluene, ethylene, propylene and styrene monomer (SM) have all also risen over the week to Thursday.

Asia’s methyl tertiary butyl ether (MTBE) prices spiked $134/tonne in the first two days after the attacks to $857/tonne, a one-year high since September 2018.

It then fell $61/tonne on Wednesday on sharp downstream gasoline losses which took a cue from crude retreat after Saudi Arabia’s energy minister Abdulaziz bin Salman reassured the markets that the Kingdom’s oil production would be back online by the end of September.

Saudi Arabia’s crude oil output was at 9.8m barrels a day on 13 September, the day before the attacks happened.

Bin Salman on 17 September said that Saudi Arabia’s average oil production in September and October would be 9.89 million barrels per day in September and October.

The International Energy Agency on 18 September also said that it does not see a need to release emergency oil stocks as markets are well supplied.

Saudi Arabia’s defence ministry late on Wednesday said that 18 drones and seven cruise missiles were fired from a direction that eliminated Yemen as a source, according to media reports.

Yemen’s Iran-aligned Houthi rebels have claimed the attacks on Saudi Arabia but Iran has denied any involvement.

Petrochemical production facilities reliant on feedstock Saudi Aramco on 18 September reported that the curtailment to their raw material supplies have improved.

PE (polyethylene) prices in the Middle East and India are yet to respond to the hikes seen in China, as buyers are uncertain of the gains sustaining in the near-term.

The Middle East PE and PP (polypropylene) markets typically see trades undertaken once a month, so it is likely that October offers set to emerge later this month draw support from the gains seen in China’s import markets as a result of the feedstock disruption in Saudi Arabia.

This is also assuming that the gains in China’s PE and PP sustain until then.

Market players in India remain unclear on the near-term PE price trend as they continue to grapple with an oversupplied domestic market.

PP demand in the Indian domestic market has, however, strengthened, with domestic supply tightness also supporting the uptick in buying.

Spot offers remain scarce as much of the business for September has been completed earlier, and those for October is yet to begin.

Major suppliers in the GCC have also sold out September allocations, limiting import activity during the week.

Asian naphtha prices were trading at $519.75/tonne CFR Japan at midday on Thursday, up $46/tonne from 13 September, as trade throughout the week remained volatile.

Naphtha prices saw its biggest single-day spike on 17 September, driven by physical buying alongside strong gains in oil prices, but slumped on 18 September tracking the drop in crude oil futures.

Ethylene sellers in Asia have retreated to the sidelines due to the volatile upstream and downstream prices, curtailing trade.

Prices of HDPE pipe grade natural 100 resin in domestic China increased by around yuan (CNY) 400-500/tonne or more and spot offers of HDPE pipe grade black 100 resin were heard to have increased by $10-40/tonne in southeast Asian markets.

Spot offers of PET from China increased to around $910-925/tonne FOB China early in the week following the steep increases in feedstock MEG.

For caprolactam, selling ideas for import cargoes were higher following the increase in benzene prices, but buying ideas remained low amid low liquidity in the downstream nylon markets.

KEY FEEDSTOCKS MOSTLY HIGHER IN ASIA

With additional reporting by Clive Ong, Keven Zhang, Judith Wang, Cindy Qiu, Veena Pathare, Zhi Xuan Ho, Hazel Goh, Yeow Pei Lin and Ai Teng Lim

Focus article by Nurluqman Suratman

Click here to visit the Saudi Arabia refinery attacks topic page

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE