China chems demand, prices and operating rates suffer as coronavirus persists

Will Beacham

21-Feb-2020

BARCELONA (ICIS)–Coronavirus continues to wreak havoc on China’s chemicals industry, though there are early signs of recovery in demand for the polyolefins sector.

Although the country’s central government is easing restrictions on logistics and the movement of people, millions of migrant workers remain stranded or in quarantine.

Industrial value chains are still being disrupted with factories crippled by lack of raw materials, manpower, high inventories, and poor downstream demand.

As newly confirmed cases of coronavirus outside Hubei continue to decline, policies have been introduced to help workers return, including toll-free motorways, special trains, and recruitment subsidies.

However, analysts at TS Lombard estimate the labour return rate of manufacturing workers is still as low as 35%, and that it is unlikely to rise above 70% before the beginning of March.

“In other words, factories might be open, but they remain empty,” economist Davide Oneglia said in a paper publised on Friday.

With China such an important part of many global supply chains, lack of components is now hindering automotive production in Europe, with Jaguar Land Rover revealing this week that they are being forced to fly parts over in briefcases to keep maintain production in the UK, according to the Financial Times.

Business operations at Hubei – the epicentre of the coronavirus outbreak in China – will not resume until 11 March, a further delay from the 21 February schedule, as the number of infections and deaths continue to spike in the central province.

Nissan and Honda are delaying restart of their automotive operations there.

Apple also reported problems getting its plants in China restarted because of personnel shortages, and warned that demand in China has fallen, meaning it will miss its global quarterly earnings target.

CHEMICALS SUFFER

In

chemicals markets, many prices are falling as a

result of poor downstream demand, with

factories cutting operating rates or delaying

post new-year holiday restarts.

China’s styrene value chain is suffering, with storage tanks for imports near full capacity and average operating rates for downstream polystyrene (PS) and acrylonitrile-butadiene-styrene (ABS) at 50.1% and 56.7% respectively, according to ICIS data.

Click on image to enlarge

–

Expandable polystyrene (EPS) price discussions

in southeast Asia slid on improved

Chinese supply, even as grocery deliveries and

pre-Ramadan restocking led to healthier demand.

Asian sellers were willing to lower offers as Chinese supply improved with some factories resuming operations.

BD INVENTORIES

RISE

Butadiene (BD) investories

have piled

up, with the resulting oversupply likely to

remain until the second quarter.

Producers in key downstream markets such as styrene butadiene rubber (SBR), polybutadiene rubber, and acrylonitrile butadiene styrene (ABS) plants are running at reduced rates.

Spot domestic BD supply is also increasing as trial runs have started at Zhejiang Petrochemical’s 200,000 tonne/year plant since December 2019, while Hengli Petrochemical’s 140,000 tonne/year unit recently started up.

The situation is also hurting broader Asian BD markets which rely on exports to China, as well as the automotive sector which as been in decline since 2019.

Supply is rising across Asia thanks to a new joint venture 185,000 tonne/year BD plant in Pengerang, Malaysia owned by PETRONAS and Saudi Aramco which came on stream late last year.

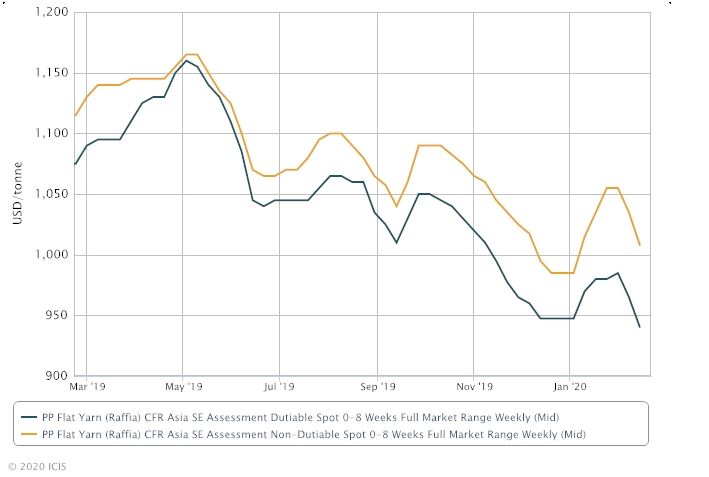

ASIA PP HIT BY REDIRECTED

CARGOES

Southeast Asian origin

polypropylene (PP) offers have

slumped as Chinese traders and suppliers

continue to offer re-directed export cargoes

from the Middle East, as well as the country’s

own local productions, to southeast Asia, in a

bid to whittle down accumulated inventory

levels.

Click on image to enlarge

–

A growing number of base oils producers in

China have

cut run rates to 60-70% or even stopped

production because of the coronavirus outbreak,

with downstream demand set to remain weak in

the near term.

Most downstream lubricant producers said their resumption of work has been delayed to mid-to-late February amid the coronavirus, pushing back base oils purchases.

POLYOLEFINS

STABILISE

Polyolefins inventories

of Sinopec and PetroChina have

fallen from their peak as downstream

customers gradually return to production.

By 21 February, inventories had dropped to 1.23m tonnes, down by 370,000 tonnes or 23% according to market sources.

Click on image to enlarge

–

Downstream producers have ramped up run rates

to around 30%, ICIS data showed.

However, there are worries that real consumption may remain low as the reduction in inventories caused by purchases for hedging low-priced cargoes.

Domestic PP and linear low density polyethylene (LLDPE) prices in east China were assessed at Chinese yuan (CNY) 6,950/tonne ($989/tonne) and CNY6,875/tonne on 20 February, rising by 5% and 3% respectively.

Click on image to enlarge

–

BRIGHT SPOT FOR

IPA

Isopropanol (IPA) prices in

Asia hit its highest in 58 weeks as demand for

the product is surging as a result of the

coronavirus outbreak.

Click on image to enlarge

–

Demand in the region, especially countries like

Malaysia, Singapore, and Indonesia, remains

strong for downstream sectors like

disinfectants, hand sanitizers/rubbing alcohol

to combat the spread of the virus.

Supply is also tight with the closure of most major Chinese plants amid the outbreak, which are major exporters in the IPA market.

Plants like Kellin Chemical and Super Chemical have shut their operations indefinitely.

Even with the restarts, operation ratios remain reduced as internal logistical issues still plague the country.

“Getting raw material [like acetone] will also be a problem,” said a Chinese producer.

($1 = CNY7.03)

Front page picture: A woman wearing a

protective face mask walks next to the China

Central Television (CCTV) building in Beijing

on Friday

Source: Roman

Pilipey/EPA-EFE/Shutterstock

Focus article by Will Beacham

Interactive content by Miguel Rodriguez-Fernandez

Additional reporting by Trixie Yap, Cheng Ran, Tina Zhang, Claire Gao, Alex Feng, Aviva Hu, Helen Yan, Leanne Tan, Min Jie Yaw, Fanny Zhang and Yuanlin Koh

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE