The three pathways to 2050 for German emissions reduction

Roy Manuell

15-Dec-2020

This story has originally been published for ICIS Long-Term Power Analytics subscribers on 17 November.

Germany’s pathway to emissions reduction by 2050 will heavily depend on carbon prices, technology developments, and climate ambition, ICIS modelling demonstrates. The findings come from our 2050 long-term power forecast that launched on 16 November across five EU countries and includes three possible routes to 2050: a Base Case outlook, a High RES and a Low RES pathway. In our High RES scenario, German annual emissions would fall below 10 million tonnes of CO2 as early as 2040, while this does not occur until 2049 in our Base Case. In our Low RES, Germany emits close to 40 million tonnes of CO2 in 2050.

The 2050 scenario assumptions

- In the High RES scenario, we assume higher carbon prices, a shorter lifetime for gas capacity and faster renewable expansion relative to our Base Case. We assume a coal and lignite phase out by 2034. We also assume carbon capture and storage for gas capacity to grow from 2030 but from 2040 in our base case

- In the Low RES scenario we assume a lower carbon prices and a slower phase-out of gas capacity than our Base Case. In both the Low RES and base case scenarios all coal and lignite capacity closes by 2038 in line with German legislation

- We have built an investment model for renewable growth that forecasts capacity expansion for onshore and offshore wind and solar technologies from 2025 onwards that takes into account technology-specific cost assumptions, geographical limitations and power sector modelling

- For each scenario we keep fuel prices constant but consider very different carbon price scenarios

Analysis

Coal and lignite

- In our High RES scenario, the much stronger

carbon price and faster renewable capacity

buildout leads to very low load factors for

coal and lignite after 2030, compounding the

emissions reduction due to the earlier capacity

phase-out by 2034

- For example, we see the average yearly load factor for lignite falls below 30% from 2031 onwards and that of hard coal plants average well below 40% for the same period

- Carbon prices begin to gather significant momentum in our High RES scenario from around 2030 onwards, cutting into the profitability of lignite in particular as the most carbon-intensive fuel in the German mix

- In our Base Case Base we again see low load

factors in the 2030s due to high carbon prices,

though to a lesser extent than in the High RES

scenario

- The average yearly load factor for lignite remains above 30% between 2030 and 2038 when the technology is fully phased out

- In our Low RES scenario, with the slowest

renewable capacity build out and more moderate

carbon price environment, coal and lignite

generation remains strong until the phase-out

that also takes place in 2038

- Lignite plant load factors remain well above 80% in the 2030s in our Low RES

- As a result, the differences between the three pathways in terms of coal and lignite generation is very significant from 2030 onwards but more marginal in the 2020-2030 period

Renewables

Renewables

- Renewable generation differs across the three pathways in our investment model that adds subsidy-free renewables from 2025 onwards

- The High RES scenario assumes the lowest Levelised Cost of Energy (LCOE), the fastest technology learning rates and is least restrictive scenario in terms of natural boundaries to expansion (physical land space is one example). The Low RES assumes the opposite, with the Base Case between the two

- When combined with the other

scenario-specific assumptions in our Horizon

model, this leads to very different renewable

capacity build out pathways that ultimately

enables a much faster transition to clean

electricity production in the High RES scenario

- In 2030, the renewable share of generation is similar in each scenario at around two thirds, but by 2040 this is 92% in our High RES pathway, 89% in our Base Case and 68% in our Low RES as the impact of the investment model assumptions takes effect

- By 2050, this is 93%, 93% and 74% respectively

CCS and

gas

CCS and

gas

- A significant contribution to the emissions

reduction comes from the different capacity

pathways for carbon capture and storage (CCS)

- In our High RES scenario, CCS gas capacity is installed from 2030 but not until 2040 in our Base Case, and not at all in out Low RES scenario

- CCS capacity in the High RES has a strong impact on emissions reduction due to rapid capacity expansion in the 2030s that sees CCS gas generation overtake non-abated gas production in 2037. This happens a decade later in our Base Case

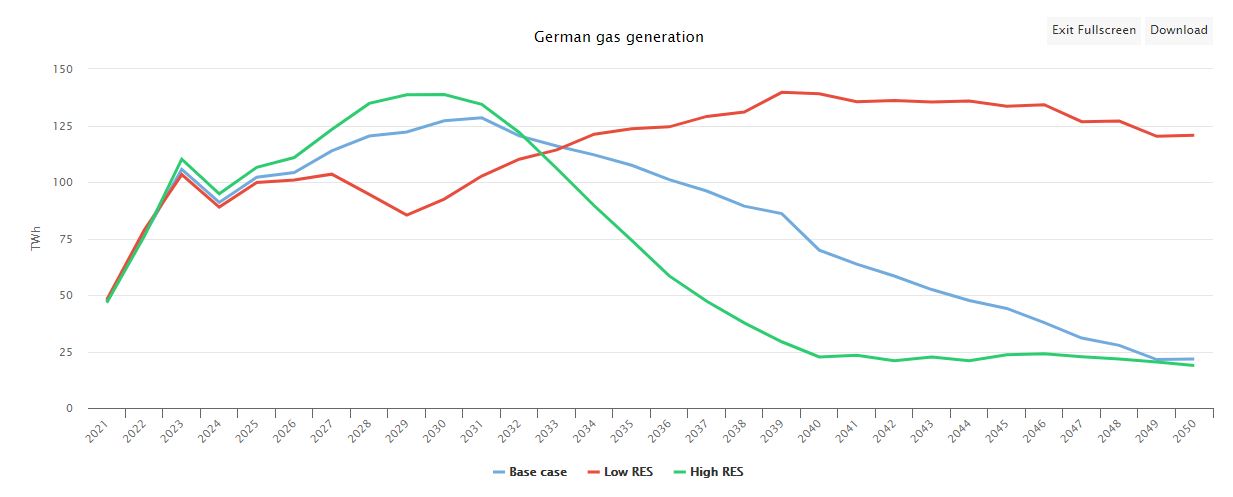

- As a result of gas, coal and lignite

capacity assumptions, renewable capacity build

out, as well as CCS, gas-fired generation

differs significantly across the scenarios

- We assume a gas plant lifetime of 30 years in our High RES, 35 years in the Base Case and 40 years in the Low RES

- In the High RES scenario, gas generation initially rises above our Base Case and Low RES scenarios in the 2020s due to a higher rate of fuel switching from coal to gas

- From the early 2030s onwards, gas-fired

generation in the High RES scenario then falls

below the Base Case due to the introduction of

CCS and faster rate of renewable expansion and

gas capacity closures

- This sees the load factor rapidly fall in the High RES pathway from close to 40% at the end of the 2020s to below 30% in 2035, compared to a relatively stable and steady decline in the Base Case through to 2050

- Gas-fired output rises steadily to 2040 in our Low RES pathway and in the year 2050 generates around 100TWh more power than in our Base Case and High RES scenarios

Emissions

Emissions

- Overall, our findings demonstrate three distinct pathways to 2050 in terms of emissions reduction but in the case of the High RES and the Base Case, similar end points

- While the High RES pathways reduces annual

emissions to below 10 million tonnes as early

as 2040, this does not take place until 2049 in

our Base Case, though both have very similar

emissions totals in the year 2050

- The High RES scenario reduces emissions a lot faster due to the greater climate ambition of carbon prices and capacity changes

- Our Base Case is relatively more moderate

- The High RES scenario results in an overall emissions saving of 300 million tonnes between 2031 and 2050 compared to the Base Case

- In stark contrast, the Low RES pathway

still sees 37 million tonnes of CO2 emitted in

the year 2050, with a total of 670 million

tonnes more carbon produced between 2031 and

2050 than our Base Case

- On the closure of all coal and lignite capacity in the Low RES scenario, emissions halve from 90 million tonnes in 2038 to 43 million tonnes of carbon the following year

- As with other differences between the three

scenarios, in 2030 emissions are relatively

similar, in particular between the Base Case

and High RES in which the latter emits just 2

million tonne less of carbon

- By 2040, less than half as much CO2 is emitted in the High RES relative to the Base Case whereas the Low RES produces roughly twice as much carbon as the Base Case

- By 2050, the Base Case and High RES have very similar annual emissions totals

Our ICIS

Long-Term Power Analytics customers have access

to extensive modelling of different options and

proposals. If you have not yet subscribed to

our products, please get in contact with Justin

Banrey (Justin.Banrey@icis.com)

or Audrius Sveikys (Audrius.Sveikys@icis.com).

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE