Sky high chemicals prices may stoke downstream inflation

Will Beacham

14-May-2021

BARCELONA and LONDON (ICIS)–Rising chemical prices around the world may be helping to stoke inflation in downstream industrial production and consumer goods.

Since the pandemic hit in early 2020, a series of events have disrupted supply of chemicals to global markets amid strong demand, leading to record prices in some value chains.

As demand fell for transport fuels in the first half of 2020, refineries closed down or reduced run rates. This reduced supply of feedstocks such as naphtha and propylene for chemicals production.

Also in 2020, the US’ hurricane season, followed by the February 2021 polar storm, closed down large parts of the US chemicals sector.

In the aftermath of the polar storm, 100% of US capacity was offline for some important products such as butadiene (BD) and polycarbonates (PC).

Repairs and restarts have taken several months and not all have been completed.

The global container crisis has also disrupted chemicals supply. Normal flows of products have been delayed or cancelled due to a lack of available capacity, and prices that have spiked to unsustainable levels, according to market participants.

The China to Europe route has been particularly badly hit.

Some European chemical markets have become stranded by the current supply chain disruption, made worse by the closure of the Suez Canal at the end of March.

The container supply chain crisis is expected to last at least until the third quarter of 2021.

Europe has also been hit by a series of unplanned production outages which have resulted in a large number of force majeures this year.

Currently, 27 locations are affected by force majeures, compared with 14 at the same time last year, and seven in 2019.

Europe also has a large number of planned maintenances underway, which are taking further capacity offline.

Some of these were delayed from 2020 by the pandemic.

Planned, unplanned ethylene outages in Europe

Against this background, prices along some European value chains have reached their highest levels this century.

DEMAND IS STRONG

Demand

has also surprised on the upside, driven

initially by products to fight the coronavirus

as well as plastics for packaging.

Since the second half of 2020 there has also been a strong rebound in demand from big end use sectors such as automotive and construction, battered by lockdowns in the early months of the pandemic.

China led the recovery, followed by the US and Europe.

“Demand for chemicals is booming globally, led by a recovery in industrial production,” said ICIS lead demand analyst, Rhian O’Connor.

“Global industrial production for Q2 2021 is 15% higher than the same period last year, and an incredible 4% higher than 2019, according to Oxford Economics. This means essentially that not only has chemicals demand recovered, it has actually grown from pre-pandemic levels.”

In markets starved of material, there has been panic buying by downstream industries desperate to maintain security of supply.

In these circumstances, availability has become more important than price, leading to record prices in many products.

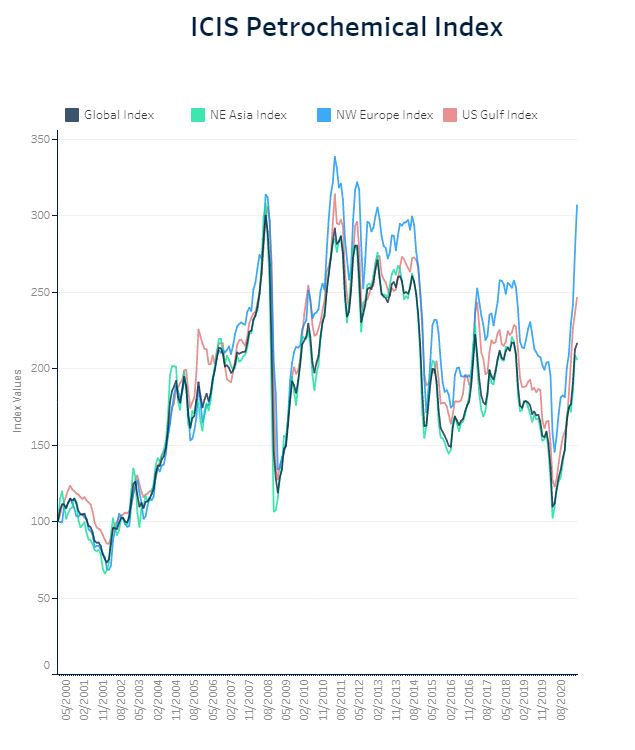

The ICIS Petrochemical Index tracks chemical prices in important value chains and regions. After collapsing in early 2020 during the first wave of pandemic lockdowns, the data for April shows there has been a sharp bounce back in petrochemical prices across all regions, led by northwest Europe and the US Gulf.

Europe chemicals prices have now spiked to 2013 levels, when Brent crude oil was over $100/bbl.

There is usually a close relationship between chemical and crude oil prices. There is also a record gap between Europe and the other regions, illustrating how it has been effectively cut off from global imports.

US prices have reached levels last seen in 2014, while in Asia prices have peaked and are now falling.

China’s economic growth has slowed, and exports to Europe have been hit by the disrupted supply chain to Europe. The resurgent pandemic in India and southeast Asian countries is also hurting demand and sentiment there.

EUROPE SUPPLY

CHAOS

Chemical distributors in

Europe consulted by ICIS confirmed that supply

chains are stretched, with downstream customers

still in panic buying mode.

Desperation for product is driving over-ordering that it is pumping the market up to potentially third larger than its actual size, according to Frank Schneider, an executive at the Netherlands-headquartered chemicals distributor IMCD.

“I do believe that the supply chain is at the moment a bit blown up and is bigger than the normal market requirement. I do not believe that the market has grown 20-30% in the quarter,” he added.

Key raw materials are extremely short at present, throttling production and spiking prices all along the value chain, down to the consumer.

“Key raw materials have suddenly gone incredibly short and we have customers who’ve been ignoring us for years literally begging for material,” said Richard Gilkes, managing director of UK-headquartered Stort Chemicals.

Europe’s force majeures have further exacerbated the tightness, along with supply chain disruptions that could be set to continue through the rest of this year.

“This is the main pain point for all of my colleagues at the moment, dealing with delays, with changing orders, with new information coming in,” said Gerd Bergmann, CEO of distributor Nordmann.

“Every morning you have a different situation.”

Raw materials prices are also expected to remain high, but the upticks in oil pricing and demand as vaccination programmes continue to roll out is likely to cause a significant ramp-up in refinery output in the next few months, according to the International Energy Agency (IEA) this week.

Underlying demand is driven by more than fly-up margin and shortages, according to Bergmann.

“I think all producers have been caught by surprise by the ramp-up of the demand, but I think that this demand is solid,” he said.

“There is some stockpiling still, and maybe that will level off, but I think we can say now that we are maybe back to a solid situation.”

Despite the eurozone slipping back into recession in the first quarter of the year, demand has been rebounding largely since the end of the first European lockdowns in mid-2020 and has trended bullish throughout despite the jagged arc of country recoveries, punctuated by spikes in infection rates.

Eurozone manufacturing has been driving overall private sector growth since the third quarter of 2020, and chemicals production has significantly outperformed general industrial growth in March, expanding 1.1% month on month compared to 0.1% for the manufacturing sector as a whole, according to Eurostat.

With economies in the developed world continuing to open up, demand is likely to continue strong as economies push closer towards a point that could resemble normality.

The travails of and lack of support given to the developing world is likely to cast a shadow for years to come, however.

“Today’s prices are the result of shortages of commodities supply, for example in petrochemicals, very strong demand and supply chain disruptions,” said ICIS senior consultant for Asia, John Richardson.

“I am beginning to believe that the latter is the biggest reason for commodity price inflation, which is feeding through into sharp rises in the cost of finished goods – and a lack of goods availability.”

SUPPLY/DEMAND

BALANCING

Once the current supply disruptions draw to a

close, real underlying supply and demand are

likely to become more balanced, reducing the

the pressure on price inflation.

For ethylene – a key building block chemical for manufacture of packaging materials – record high amounts of ethylene capacity is being added in 2021 and 2022, predominantly driven by northeast Asia.

“China ethylene capacity is forecast to more than double between 2019 and 2025, which will outstrip demand growth, leading to depressed operating rates,” concluded ICIS analyst James Wilson.

Global ethylene operating rate

Focus article by Will Beacham and Tom Brown

Interactives by Miguel Rodriguez-Fernandez and Yashas Mudumbai

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Now, more than ever, dynamic insights are key to navigating complex, volatile commodity markets. Access to expert insights on the latest industry developments and tracking market changes are vital in making sustainable business decisions.

Want to learn about how we can work together to bring you actionable insight and support your business decisions?

Need Help?