INSIGHT: Regional olefins and PE margins shift markedly on feedstock cost increases

Nigel Davis

13-May-2022

LONDON (ICIS)–Despite the magnitude of feedstock cost increases being essentially the same in both regions, the differences between margins for producers of polyethylene in Europe and northeast Asia remain stark.

Producers in Asia have not been able to pass on higher feedstock costs in product prices downstream, a symptom of unbalanced markets and the China slowdown which continues to be exacerbated by the country’s harsh COVID-19 containment policy.

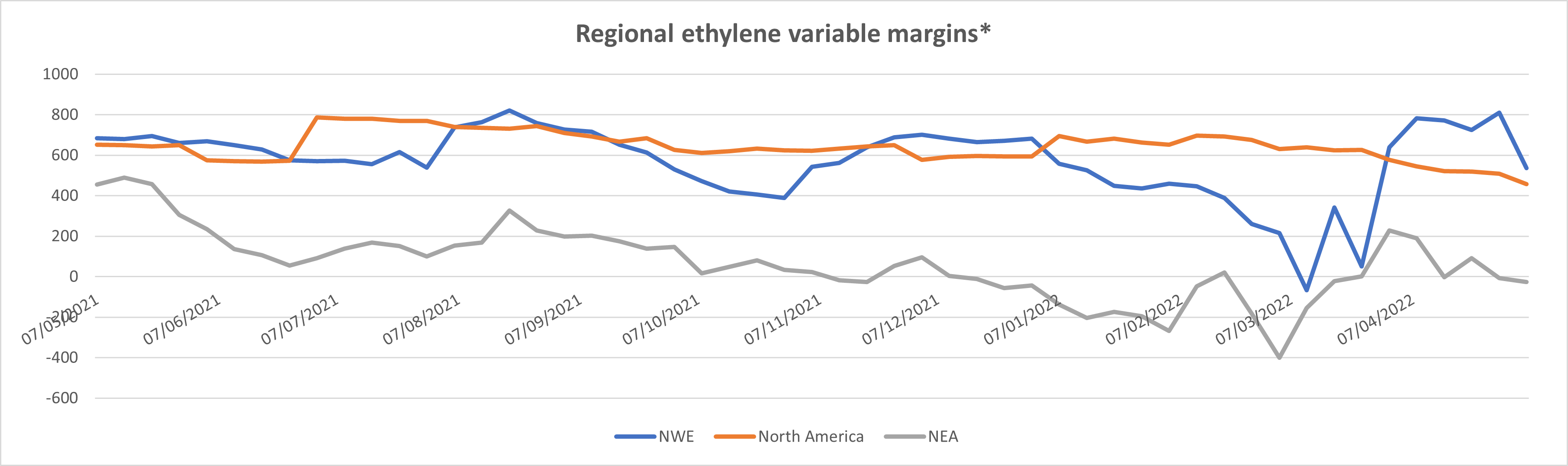

ICIS data show how rising costs for cracker operators and polymer producers have fundamentally shifted costs curves in a few months. Earlier, relatively stable and flat curves have given way to more significant differences between variable costs of production among market participants.

Click on image to enlarge

This is a consequence of sharply increased crude oil and hence naphtha costs which in Europe have rather successfully been passed to the downstream. In Asia this has not been the case with relatively lower PE prices hitting sector players hard and putting intense negative pressure on margins.

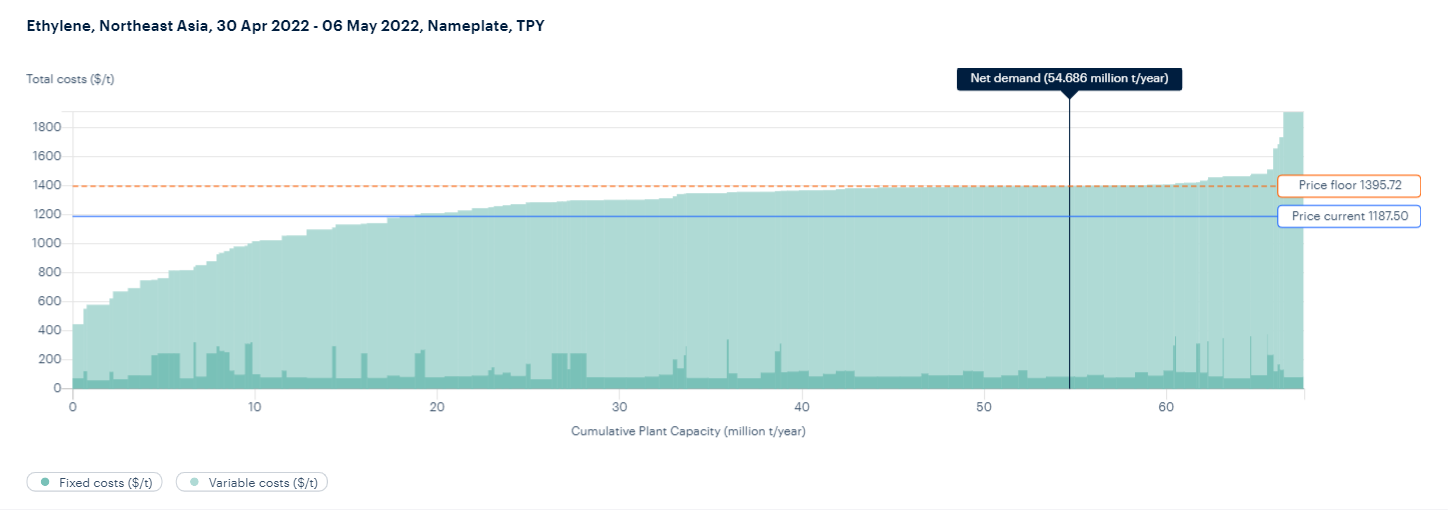

The ICIS Plant Cost Evaluator (PCE) shows how ethylene prices in early May were not covering costs for many crackers in northeast Asia and a steep cost differential at the low-cost end of the cost curve.

Click on image to enlarge

The picture in northwest Europe was very different with supply and demand better balanced and many crackers operating theoretically in positive territory.

ICIS margin data show that high density polyethylene (HDPE) margins in NE Asia dipped negative in October last year and have dropped further at times since.

This is a clear result of China’s slowdown and the impact on petrochemicals. That situation is exacerbated now by the country’s zero-COVID policy and lockdowns that are hobbling manufacturing industry as well as more nuanced consumer demand.

Click on image to enlarge

*US$/tonne

Source: ICIS

Significant pressure on demand growth is worsening with some scenarios suggesting that demand for the major polymers might shrink this year.

Earlier growth assumptions are being continually re-assessed against the backdrop of China’s COVID-19 battle and Russia’s war in Ukraine.

Shifting balances of supply and demand are likely to keep a cap on prices in Asia and producers’ ability to pass on higher raw material and energy costs.

Click on image to enlarge

*US$/tonne

Source: ICIS

In Europe, feedstock costs have been passed on in higher prices more successfully through the cracker to the polymer and this has altered the margin picture relative to other parts of the world.

Ethane costs have been rising for US cracker operators putting a squeeze on margin. For HDPE the higher ethylene price has been a feature since the second half of March. Ethane prices in the US in early May were their highest since 2012.

The data create a striking picture of ethylene margins (from the cracking of naphtha in northwest Europe) based on monthly contract prices pushing above those for the cracking of ethane in the US through April and into the beginning of May.

Northwest Europe HDPE margins have moved higher too but have remained eclipsed by margins for producers on the US Gulf.

Insight by Nigel Davis

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE