NPE ’18: Constrained global supply, strong demand weigh on US nylon

Lucas Hall

07-May-2018

HOUSTON (ICIS)–The US nylon 6 and nylon 6,6 markets continue to face upward pressure despite decreasing feedstock costs amid severely constrained global supplies and strong global demand, heading into this year’s National Plastics Exposition (NPE).

US nylon 6 supplies remain constrained following production issues in the first quarter, in addition to an increase in demand associated with severe supply shortages and production issues in the global nylon 6,6 market.

BASF declared force majeure on North American nylon 6 production from 16 January through 28 February amid cold weather conditions that disrupted production at a number of plants in the southern US. Although production has returned to normal, supplies remain tight on strong global demand.

Meanwhile, buying demand for nylon 6 has increased, as a number of typical nylon 6,6 users have switched to buying nylon 6 where substitution is available due to disadvantageous nylon 6,6 prices associated with severe supply shortages and production issues, primarily in Europe.

One distributor noted that it was “out of nylon market” because it “can’t get any at reasonable price”.

Higher feedstock costs and production issues have also weighed on the market.

CITGO had a leak at its cyclohexane (CX) unit in April, used to make caprolactam (capro) in the nylon 6 chain. Other CX production issues have been heard but remain unconfirmed in the market.

Although primary nylon 6 feedstock benzene contract prices in the US have seen steady declines since December following an upward trend for most of 2017, the December increases are still being felt downstream.

One producer noted: “The benzene drop over the last five months still hasn’t offset the spike up in December.” Moreover, initial expectations are that contracts will settle up for June based on higher crude prices, putting upward pressure still on downstream nylon 6.

Although no formal announcements have been made, price increases are being discussed, with one producer noting: “Demand is as strong as it ever has been.”

As such, freely negotiated prices for US nylon 6 are expected to continue to trend up so long as feedstock costs remain elevated and supplies remain snug.

The US nylon 6,6 faces similar, if not more severe, concerns, as global supply has been significantly constrained for months amid ongoing production issues, namely in Europe.

Major US nylon 6,6 producer Ascend Performance Materials was on turnaround for feedstock acrylonitrile (ACN), used to make adipinotrile (ADN) in the nylon 6,6 chain, during Q2 2017 before Hurricane Harvey battered ACN production in the US Gulf in the third quarter.

The storm prompted the company to declare force majeure on US ACN until 1 November and severely depleted feedstock availability for internal consumption in the nylon 6,6 chain. Although the producer is operating at high rates, inventories remain limited.

Ascend also declared force majeure on feedstock hexamethylene diamine (HMDA) at its Decatur, Alabama facility in January due to cold-weather related issues in January. Although the company lifted force majeure as of 1 March, supply levels remain insufficient to satisfy strong global demand.

Many European producers are on force majeure for nylon 6,6 due to feedstock shortages in the region. Availability has been further hampered by ongoing rolling strikes in France, which have caused logistical delays for some players moving material from and through that region of Europe.

There are short-term signs of relief, however, despite ongoing problems in Europe.

Major feedstock ADN producer Butachimie lifted force majeure at its Chalampe, France facility in early April. Supplies are expected to improve following a period lag time in May between producers receiving additional raw materials and producing more material.

Supply should overall continue to improve slowly so long as upstream markets remain stable in terms of output and the ongoing industrial action in France does not worsen.

Meanwhile, demand remains strong, with most users selling out of product as fast as they can restock and many buyers unable to obtain material.

At the same time, much like US benzene contracts, contracts for US chemical-grade propylene, a major feedstock used by a number of producers in nylon 6,6 chain, have seen steady declines since January following a general uptrend in 2017 in the wake of production issues before and after Hurricane Harvey. However, a spike in January contracts continues to be felt in the market as prices still remain higher than pre-Harvey levels.

Despite sustained upward pressure, however, no price increase announcements have yet to be confirmed in the market.

Supplies are expected to remain severely constrained through at least May as producers work to replenish inventories alongside strong global demand.

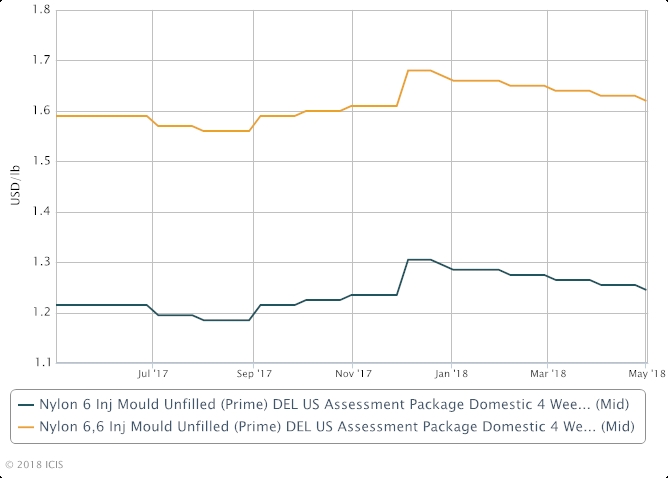

May US nylon prices were assessed on Tuesday at a 1 cent/lb ($22/tonne) decrease from April, tracking lower prices for US May benzene contracts.

ICIS US nylon assessments are formula-based and tied to movements in feedstock costs.

Nylon, also called polyamide (PA), is used mainly in fibre and engineering polymer applications. Nylon fibres are used in apparel, carpets and home furnishings. Nylon engineering resins are used in automotive parts.

Major nylon producers in the US include AdvanSix, Ascend Performance Materials, BASF and INVISTA.

Sponsored by the Plastics Industry Association (PLASTICS), NPE2018: The Plastics Show takes place on 7-11 May in Orlando, Florida.

Focus article by Lucas Hall

Global News + ICIS Chemical Business (ICB)

See the full picture, with unlimited access to ICIS chemicals news across all markets and regions, plus ICB, the industry-leading magazine for the chemicals industry.

Contact us

Partnering with ICIS unlocks a vision of a future you can trust and achieve. We leverage our unrivalled network of industry experts to deliver a comprehensive market view based on independent and reliable data, insight and analytics.

Contact us to learn how we can support you as you transact today and plan for tomorrow.

READ MORE