China could either see average annual net imports of 5m tonnes in 2024-2030, net exports of 2m tonnes a year or be in a balanced position. A lot will depend on trade barriers.

Asian Chemical Connections

Details of how Saudi Aramco COTC and other advantaged feedstock projects could redraw the petrochemicals map

There is a big new wave of lower-carbon and very advantaged cracker projects on the way, including Saudi Aramco’s crude-oil-to-chemicals investments.

Global chemicals: What I believe our industry must do in response to a deep and complex crisis

I WORRY that we face a crisis deeper and more complex than any of us have seen before because of the confluence of geopolitics, demographics, the changing nature of the Chinese economy as Common Prosperity reforms accelerate, China’s rising chemicals and polymers self-sufficiency, the high levels of global inflation with all its causes, and, last but certainly not least, climate change.

Chemicals companies face an unprecedented demand and supply crisis

THE GLOBAL CHEMICALS industry is, I believe, facing a demand and supply crisis on a scale and on a level of complexity that nobody has experienced before. This is a huge subjects requiring a series of posts. Let me start by looking at China’s role in this crisis. In later posts.

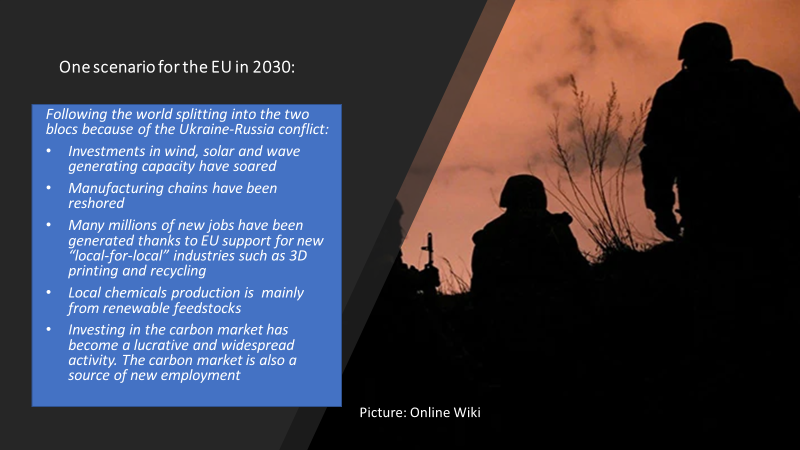

The EU in 2030: How Ukraine-Russia could reshape its chemicals industry and economy

”. Manufacturing cost pressures and the climate change and plastic -waste clean-up imperatives have created a new chemicals business model. No longer is financial success driven by sales-volume growth in chemicals.

Geopolitics have always shaped the petrochemicals industry

THE HEADLINE IN the above slide has always been the case. But why it was forgotten could be because many of us spent most, if not all, of our professional careers in the benign period between the end of the Cold War in 1991 and the pivot in the US approach to China, which happened some four years ago.

China quarter-on-quarter data finally confirms loss of growth momentum

By John Richardson WE WILL CONTINUE to stumble around in the dark unless we gain a much better understanding of the new variables that are shaping the petrochemicals business. As I’ve been discussing since last August, one of the grey areas is demand and how it has been reshaped by the pandemic, on top of […]

Global supply chain disruptions may maintain, or even add to, regional petchem imbalances

By John Richardson THE GLOBAL petrochemicals business looks set to remain largely in the dark about what will happen next to container freight and semiconductor supply. This a new area of risk for producers and buyers that highlights the need for much better analysis and data on the pandemic’s impact on markets. Let me begin […]

Petrochemicals demand and the pandemic: we continue to stumble around in the dark

By John Richardson THE BIGGEST UNKNOWN out there remains whether petrochemicals and polymers demand will be stronger, the same or weaker post-pandemic than during the pandemic in the developed markets plus China. We seem to be getting no closer to any answers. This matters from a hard-hearted dollars and cents perspective because the developed markets […]

Seeing through the lack of data: new scenarios for global LLDPE demand in 2021-2025

By John Richardson WE DON’T HAVE THE DATA sets nor the data tools to work out what is going to happen next with any acceptable degree of reliability. Until or unless we develop the necessary data sets and tools we will remain, in my view, all at sea about the direction of petrochemicals demand. The […]

Jump to page: