Chemicals companies need to decide where they are heading now that the Supercycle is over

Asian Chemical Connections

Petrochemicals three years from now: A shrinking global market?

MORE THAN 70% of global polyethylene demand is at risk from ageing populations, climate change and geopolitics.

Supermajors versus Deglobalisation scenarios: The impact on petrochemicals and recycling

THERE ARE TWO scenarios or roads down which the petrochemicals industry could travel over the next ten years, with arrival either at Supermajors or Deglobalisation.

Winners and losers as demographics, debt, sustainability, geopolitics and crude-to-chemicals rewrite the rules of success

I BELIEVE WE are heading for the biggest period of change in the global petrochemicals industry since the 1990s.

This was when globalisation took off with the formation of the World Trade Organisation (WTO), when China’s economic boom began, when the global population was more youthful and before climate change became a major threat to growth.

Demographics, sustainability and 1bn tonne less global polymers demand

Flat 2023-2050 demand growth in China and the developed world would leave the global market for nine synthetic resins 1bn tonnes smaller than the ICIS base case.

If you think this is a typical chemicals downcycle, think again

THERE IS A FEELING out there that the chemicals and polymers industry is undergoing a typical downcycle that will last a few years, followed by yet another spectacular fly-up in margins. But I believe a great deal more is happening beyond the usual cycles of over-building followed by under-building.

Global chemicals: What I believe our industry must do in response to a deep and complex crisis

I WORRY that we face a crisis deeper and more complex than any of us have seen before because of the confluence of geopolitics, demographics, the changing nature of the Chinese economy as Common Prosperity reforms accelerate, China’s rising chemicals and polymers self-sufficiency, the high levels of global inflation with all its causes, and, last but certainly not least, climate change.

Global chemicals face negative growth on inflation, more logistics problems and a deep China downturn

SUPPLY-CHAIN problems continue to disrupt the global chemicals and polymer industries more than two years since the pandemic began.

Right now, the centre of attention of supply-chain anxiety is China.

Europe petrochemicals demand weakness may have bigger impact than any production cuts

Lower refinery operating rates on a lack of Russian oil and naphtha -– and reduced electricity supply to refineries and petrochemicals plants -– may be more than offset by weaker European petrochemicals demand.

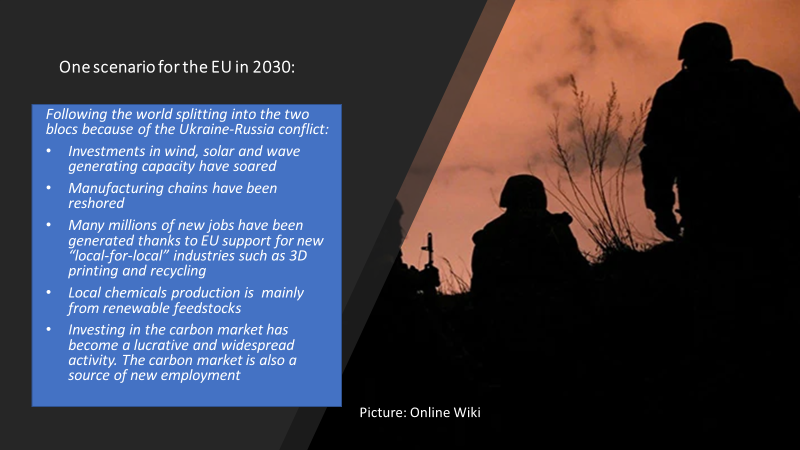

The EU in 2030: How Ukraine-Russia could reshape its chemicals industry and economy

”. Manufacturing cost pressures and the climate change and plastic -waste clean-up imperatives have created a new chemicals business model. No longer is financial success driven by sales-volume growth in chemicals.

Jump to page: