THE THREE EVENTS described are historic, meaning that the tremendous volume growth that the petrochemicals business has seen since 1992 could be largely over.

The focus therefore needs to switch to growing value

Asian Chemical Connections

CFR China PE spreads hit a new record low because of all-time high oversupply

So far in 2024, despite supply tighter than it was in December last year, the average per tonne CFR China PE price spread over CFR Japan naphtha costs has fallen to its lowest annual level since we began our price assessments way back in 1993. 2022 and 2023 were the previous record lows.

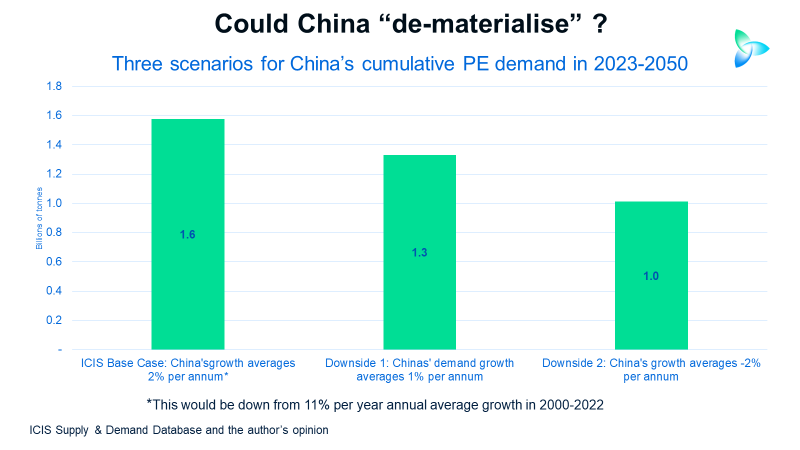

China’s one-off PE demand boom and why consumption could now shrink

The ICIS Base Case is already very conservative, assuming an annual average China PE demsnd growth of just 2% per year between 2023 and 2025 compared with 11% in 2000-2022. But I see average growth of only 1% or even minus 2% as perfectly possible.

China PP demand could grow by 3% in 2023, down from the 2000-2020 average of 10%

THE EARLY DATA suggest that China’s polypropylene (PP) demand could grow by 3% in 2023. This would be in line with the base case forecast I provided in February.

China PE and PP downcycle a long, long way from being over

The average China PE spread between 1 January and 17 March this year was just $290, the lowest since our assessments began.

Between 2000 and 2021, before last year’s collapse, the annual spread averaged $532/tonne. This means that until spreads increase by 83% from their current levels, there will have been no recovery..

Why China’s HDPE demand could decline in 2023-2040

China’s cumulative HDPE demand under the downside scenario would be 97m tonnes lower than our base case. in the above chart

Why China’s 1990-2022 PP consumption could have been 300m tonnes lower without the benefit of “one off” historical trends

IF China had been a typical developing economy, as the above chart illustrates, its cumulative 1990-2022 could have been 300m tonnes smaller. As history moves forward,this suggests that China’s long-term demand growth could turn negative

China HDPE: 2023 demand and net import outlook

China’s HDPE in demand in 2023 could fall by as much as 4% over 2022. Next year’s net imports may slip to as low as 3.8m tonnes from around 5.7m tonnes in 2022.

China chemicals growth and the 20th Communist Party Congress

China’s share of global demand growth in the seven big resins jumped to an astonishing 67% in 2002-2021. Northeast Asia ex-China’s share of demand fell to minus 1% with Europe and North America worth just 4% and 2% of growth respectively. The chemicals world had become dangerously lopsided.

China PP spreads data continue to show no recovery, weakest market since at least 2003

UNTIL WE SEE a recovery in China PP-naphtha spreads during around a 12-month period to close to long-term annual averages, there will have been no complete rebound in the market. The spread so far this year at just $264/tonne is 41% lower than the previous lowest year of $447/tonne in 2012.

Jump to page: