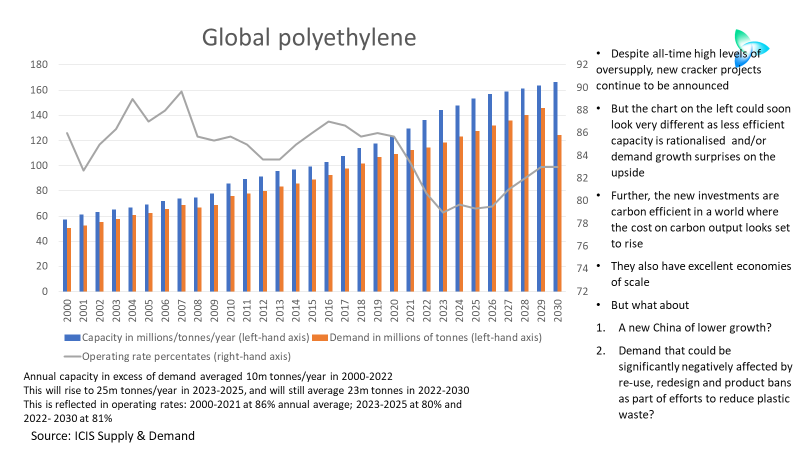

Companies behind the crackers due on-stream over the next four years emphasise the low-carbon output. The planned new plant also have excellent economies of scale

Asian Chemical Connections

Coming to terms with the new China is essential for sensible forecasting

Even our base case sees global PE capacity in excess of de</mand at 22m tonnes in 2023 compared with a 10m tonnes/year annual average in 2000-2022. We forecast this year’s global operating rate at 79% versus the average annual 2000-2022 operating rate of 86%. Downside One would see 28m tonnes of excess capacity and a global operating rate of 77%; Downside Two would be 30m tonnes and 76% respectively.

China polyolefins in 2023: Demand and supply workshops crucial

This year is a great deal harder to predict than 2022,, hence my latest outlook for China’s PP demand (see the chart below), which includes the two extremes of our ICIS base case for 6% growth versus my worst-case downside of minus 5%.

China PE market in 2023: Recovery threatened by economic inequality, real estate decline

Under Scenario 1, China’s PE demand in 2023 would total 39.1m tonnes, 4% higher than last year; Scenario 2 would see demand at 36.4m tonnes, 3% lower; and Scenario 3 would involve a contraction of 5% to 35.7m tonnes.

China HDPE 2023 demand and net import forecasts

Scenario 1 for next year assumes that China successfully transitions from its zero-COVID policies. Consumer confidence comes roaring back. Demand grows by 4% year-on-year to a market of 17.6m tonnes.

Scenario 2 assumes that high infection rates and lack of healthcare resources keep consumer confidence depressed but that the global economy recovers, supporting China’s exports. Growth is minus 2%, leaving demand at 6.6m tonnes.

The worst-case outcome is Scenario 3 where the impact of zero-COVID continues, and the global economy gets weaker. Consumption falls by 4% to 16.1m tonnes.

China LLDPE: New demand and net import outlook for 2023

China’s LLDPE demand in 2023 could either grow by 3% or contract by as much as 6%, depending on whether or not China successfully exits zero-COVID

China PP exports decline but the reason is hardly cause for cheer

In November 2021, the premium for overseas PP injection grade prices over prices in China reached a historic peak of $408/tonne. But in 1-18 November 2022, the premium was $113/tonne. Premiums have fallen in every month since April this year, resulting in a decline in China exports.

China chemicals growth and the 20th Communist Party Congress

China’s share of global demand growth in the seven big resins jumped to an astonishing 67% in 2002-2021. Northeast Asia ex-China’s share of demand fell to minus 1% with Europe and North America worth just 4% and 2% of growth respectively. The chemicals world had become dangerously lopsided.

Naphtha markets underline why “Micawberism” is not the answer

The January-September 2022 multiple of BFOE crude prices per barrel over CFR Japan naphtha prices per tonne averaged just 7.9. The lowest multiple so far this year was 6.9 in August. The January-September 2022 average was the lowest annual average since our naphtha price assessments began in March 1990.

China’s dominance of global polymer demand delivered huge global growth. But what now?

China accounted for 33% of global growth in the seven major synthetic resins between 1990 and 2001. But this jumped to 63% in 2002-2021. In distant second place during both these periods was the Asia and Pacific region at 15% and 17% respectively.

Jump to page: