China accounted for 33% of global growth in the seven major synthetic resins between 1990 and 2001. But this jumped to 63% in 2002-2021. In distant second place during both these periods was the Asia and Pacific region at 15% and 17% respectively.

Asian Chemical Connections

This is the first significant chemicals downcycle for many years

Every tonne of polymer you decide not to produce because there isn’t a viable market will save vital revenues – especially as feedstock costs will remain very volatile. Every tonne of polymer you do produce because the market works will earn you crucial money at a time of declining overall sales.

China PP spreads data continue to show no recovery, weakest market since at least 2003

UNTIL WE SEE a recovery in China PP-naphtha spreads during around a 12-month period to close to long-term annual averages, there will have been no complete rebound in the market. The spread so far this year at just $264/tonne is 41% lower than the previous lowest year of $447/tonne in 2012.

European PE and PP producers face re-globalisation risks

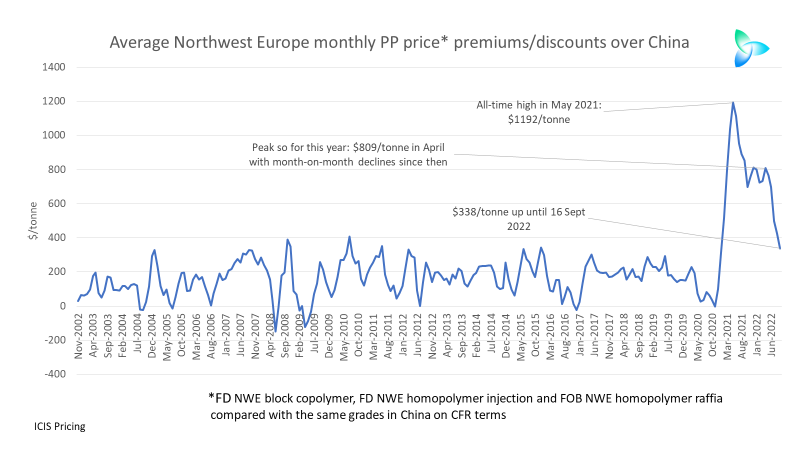

Northwest Europe PP price premiums over China averaged $161/tonne between November 2002 and December 2020. Between January 2021 and 16 September 2022, price premiums averaged $749/tonne. What would be the consequences for European PP pricing and profitability if price premiums returned much closer to their long-term averages?

China’s styrene demand in 2022 could be negative for the first time since 1990

China’s net styrene imports in 2022 could also fall to just 290,000 tonnes from 1.5m tonnes in 2021 and 2.8m tonnes in 2020.

China LDPE demand in 2022 could fall by 8%, which would be worst year since 1990

Annualised January-June China LDPE data only indicated a 4% decline in full-year demand. What a difference a month has made. The January-July numbers point to an 8% fall in demand this year. This would be the worst annual fall in growth since 1990.

If you think this is a typical chemicals downcycle, think again

THERE IS A FEELING out there that the chemicals and polymers industry is undergoing a typical downcycle that will last a few years, followed by yet another spectacular fly-up in margins. But I believe a great deal more is happening beyond the usual cycles of over-building followed by under-building.

China’s LLDPE demand weakness continues as net import prospects weaken

China’s LLDPE demand is in line to fall by 4% this year with its net imports 800,000 tonnes lower. This would follow a 1.1m tonne decline in net imports in 2021 over 2020.

The rules of the chemicals game are changing as companies pay the penalty for “growth for growth’s sake”

Because companies in all manufacturing and service sectors haven’t been adequately charged for the natural resources they use, and the damage they cause to the environment, we face the risks of catastrophic climate change and more plastic in the oceans than fish.

Global chemicals: What I believe our industry must do in response to a deep and complex crisis

I WORRY that we face a crisis deeper and more complex than any of us have seen before because of the confluence of geopolitics, demographics, the changing nature of the Chinese economy as Common Prosperity reforms accelerate, China’s rising chemicals and polymers self-sufficiency, the high levels of global inflation with all its causes, and, last but certainly not least, climate change.

Jump to page: