STRONG upside PP demand growth scenarios for the rest of the world might still not enough to cancel out negative growth in China

Asian Chemical Connections

Why China’s 1990-2022 PP consumption could have been 300m tonnes lower without the benefit of “one off” historical trends

IF China had been a typical developing economy, as the above chart illustrates, its cumulative 1990-2022 could have been 300m tonnes smaller. As history moves forward,this suggests that China’s long-term demand growth could turn negative

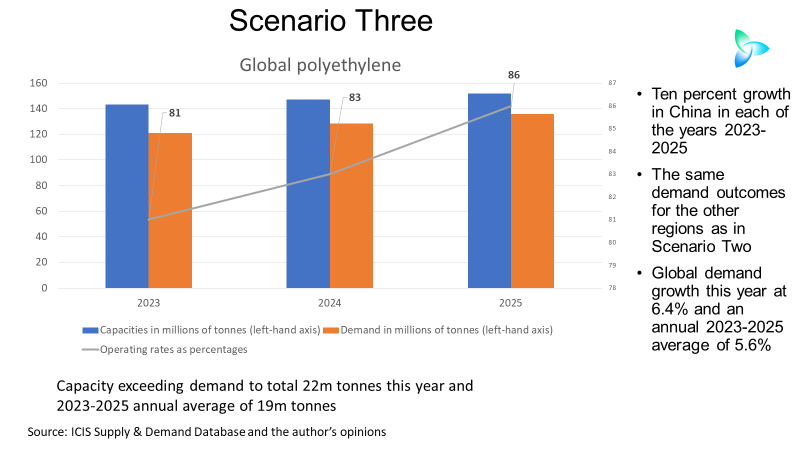

Collective wishful thinking could be behind the global polyethylene crisis

EVEN IF CHINA’S PE demand grows at 10% in 2023, with very strong growth in other regions, this year’s global capacity would still be 22m tonnes more than demand!

Interest rate “lag effect” and the risks for China’s ethylene glycols market

IT ALL CHAOS AND MUDDLE out there: China’s ethylene glycols demand could either grow by 10% in 2023 or contract by 5%.

A flood of PP no matter how what the 2023-2025 demand growth

EVEN if China’s PP demand growth is 14% this year – double our forecast – and growth in other regions is higher than we expect:

Global capacity in excess of demand would be 18m tonnes in 2023 compared with a 8m tonne/year average in 2000-2022,

Your complete and updated outlook for global polyethylene in 2023

The strength of China’s post zero-COVID recovery in 2023 will be crucial, as will local operating rates as self-sufficiency further increases.

Another important factor: European gas supply next winter and the effect on local PE production.

Assessing confidence and the China PE demand recovery: More scenarios are needed

Scenario 2, my preferred scenario, would see China 2023 PE demand at approximately 38.5m tonnes – an average of 2% higher across the three grades than in 2022.

China HDPE 2023 demand and net import forecasts

Scenario 1 for next year assumes that China successfully transitions from its zero-COVID policies. Consumer confidence comes roaring back. Demand grows by 4% year-on-year to a market of 17.6m tonnes.

Scenario 2 assumes that high infection rates and lack of healthcare resources keep consumer confidence depressed but that the global economy recovers, supporting China’s exports. Growth is minus 2%, leaving demand at 6.6m tonnes.

The worst-case outcome is Scenario 3 where the impact of zero-COVID continues, and the global economy gets weaker. Consumption falls by 4% to 16.1m tonnes.

China economy, PP demand, may see no benefit from zero-COVID exit until 2024

A SELECTIVE READING of the news is giving polyolefins market participants confidence. They see the relaxation of zero-COVID restrictions in some Chinese cities as a sign that the worst is over. But a recovery in PP and PE demand seems unlikely until 2024.

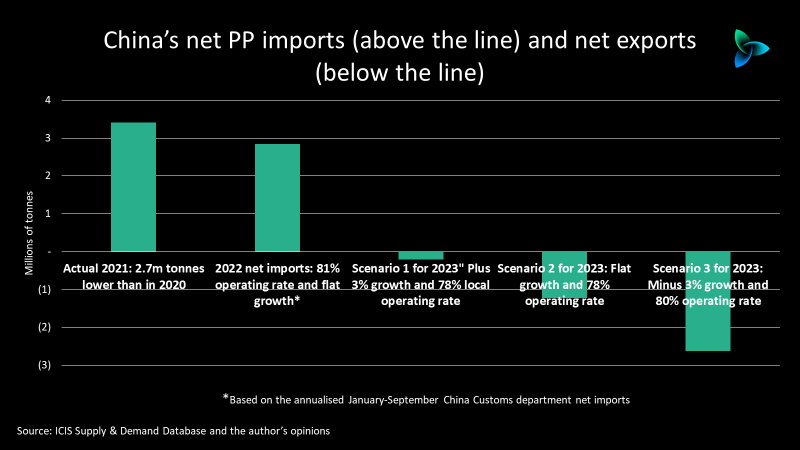

China PP demand and net import outlook for 2023

China[s PP demand growth in 2023 could be as low as minus 3% as it swings into a 2.6m tonnes net export position from this year’s likely net imports of around 3.4m tonnes.

Jump to page: