Why dig more oil and gas out of the ground to make petrochemicals when the carbon cost is potentially ruinous for our climate? This might be a question increasingly asked by legislators, shareholders and the general public – rightly or wrongly.

Asian Chemical Connections

Beware of the “head fake” of an improving China and better Q2-Q4 chemicals financial results

YEAR-ON-YEAR chemical company financial results could we improve in Q2-Q4 2023; But this should not be seen as a return to the Old Normal.

China HDPE demand set for 3% decline this year with, perhaps, overstocking supporting the other grades

CHINA’S POLYETHYLENE (PE) market has performed in a very mixed fashion so far in 2023, as the above chart tells us.

The annualised January-March 2023 data suggest a 3% fall in high-density PE (HDPE) full-year demand over 2022, a 3% in increase in low-density PE (LDPE) demand and a 4% increase in linear-low density PE (LLDPE) consumption.

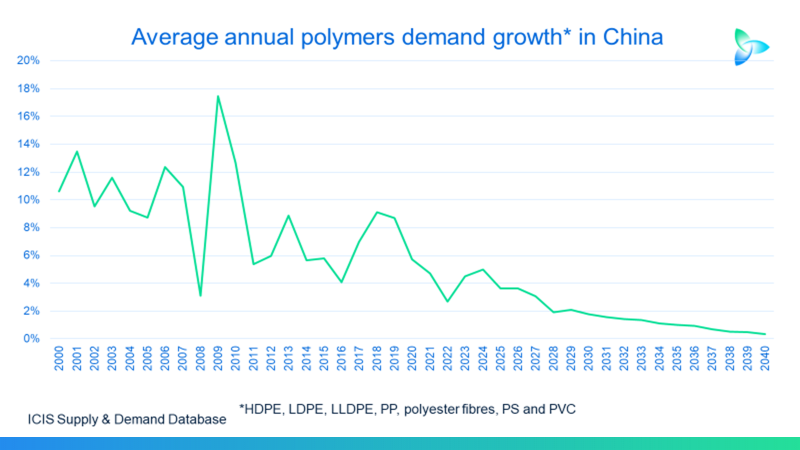

China’s one-off PE demand boom and why consumption could now shrink

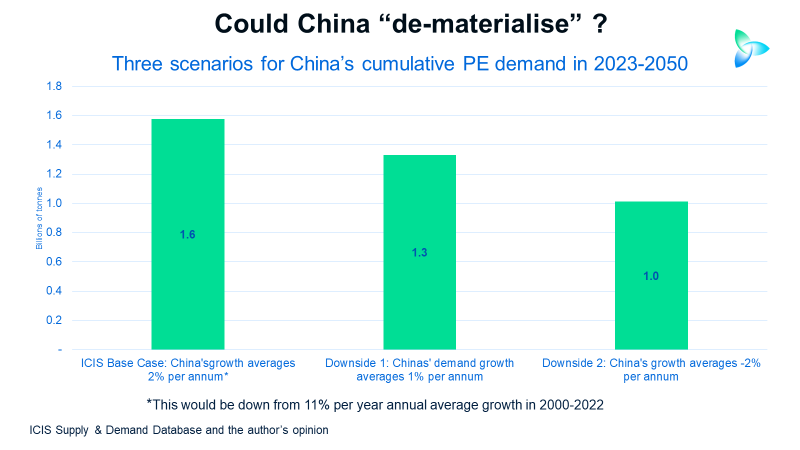

The ICIS Base Case is already very conservative, assuming an annual average China PE demsnd growth of just 2% per year between 2023 and 2025 compared with 11% in 2000-2022. But I see average growth of only 1% or even minus 2% as perfectly possible.

China PP demand could grow by 3% in 2023, down from the 2000-2020 average of 10%

THE EARLY DATA suggest that China’s polypropylene (PP) demand could grow by 3% in 2023. This would be in line with the base case forecast I provided in February.

China PE demand growth in 2023 could be only 1% versus forecasts of 5%

Early data suggest China PE demand growth in 2023 will follow the trend since 2021 of much, much lower growth.

US PE exports in 2023 are not inevitably going to increase

A SCENARIO-BASED approach is essential to understand US PE exports in 2023, based on non-plant economic factors

Why China’s HDPE demand could decline in 2023-2040

China’s cumulative HDPE demand under the downside scenario would be 97m tonnes lower than our base case. in the above chart

Global oversupply of petrochemicals to hit 218m tonnes in 2023 – the highest in any other year since 1990

Capacity exceeding demand is forecast to reach 218m tonnes this year from a 1990-2022 annual average of 76m tonnes.

Why China’s 1990-2022 PP consumption could have been 300m tonnes lower without the benefit of “one off” historical trends

IF China had been a typical developing economy, as the above chart illustrates, its cumulative 1990-2022 could have been 300m tonnes smaller. As history moves forward,this suggests that China’s long-term demand growth could turn negative

Jump to page: