By John Richardson

THE blog has been long on South Korea ever since its first visit in 1997. Its economic achievements since the horrors of the Korean War are nothing short of amazing.

Bereft of natural resources, all it has had to rely has been its intellectual capital and, wow, look at how it has progressed from the mass manufacturing of low quality finished goods to becoming the producer of globally recognised high-value electronics and automobiles. It is one of the few countries to have successfully escaped the “middle income trap”.

But now South Korea is yet another example of how demographics will shape global economic development over the coming decades.

Sure, if you want to carry on assuming that GDP growth will remain constant because there’s always “pent-up” demand, that’s fine. We worry, though, that if you do you, and you use this as the only basis for planning, your chemicals business will struggle.

This is evolving stuff, incredibly complex – and so the debate is the thing. Only through constantly reviewing where we are at will we get close to being able to estimate future patterns of demand.

And so in South Korea – as this excellent Economist article points out – some of the key variables around the impact of demographics include the success or failure of:

- Devising a workable system to pay for soaring pension liabilities.

- Persuading young people that the “lump of labour fallacy” is, indeed, a fallacy. In others words, getting the younger generation to accept that their jobs will not be threatened if more and more people are allowed to work long past the current retirement age.

- Manufacturing the finished goods that will be needed by South Korea’s ageing population. We don’t even know what these goods are yet. But South Korea, with its tremendous history of innovation, is in an excellent position to rise to this challenge.

- Retraining older people, who, in the case of South Korea, grew up in a very different world where there was no Internet, Google, Microsoft, Facebook etc.

- Persuading firms to adopt a “wage-peak” system. This involves employees draw their highest salaries during their most productive years, whenever those may be, with remuneration tapering off as their productivity declines.

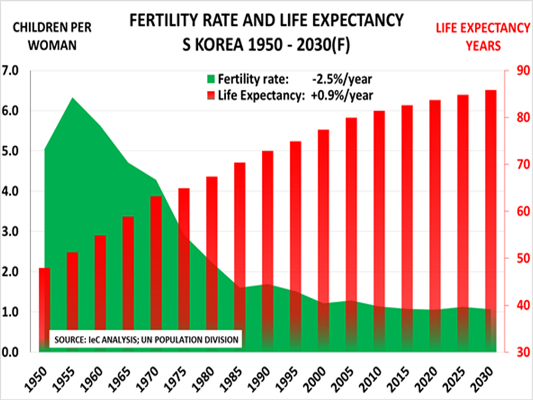

- Transferring some of the burden of childrearing from the country’s increasingly ambitious, highly educated women elsewhere. South Korea’s fertility rate, at less than 1.3 children per woman, is the lowest in the OECD (see the above chart) because balancing home life and work is very difficult for women who want careers.

This last point leads to the obvious conclusion that once South Koreans start having more babies everything will get back to normal.

True, but what about the time lag? It will take 20-30 years before any rise in the birth rate fixes the problem.

What about greater immigration and reunification with North Korea? According to The Economist, both of these would make only a marginal difference.

And so South Korea has to get on with dealing with these inescapable facts:

- The country is ageing faster than any other country in the OECD. Last year, almost 12% of the population were aged 65 or over. By 2030, that proportion will double.

- The number of South Koreans of working age will peak in just three years’ time, according to the OECD’s Randall Jones and Satoshi Urasawa. By 2040 their number will drop by about a fifth.

Burying one’s head in the sand is obviously one option, but, luckily, it looks like South Korea is adopting a very different approach.